TruePoint Insurance is one of Georgia�s fastest growing insurance agencies. We are affiliated with SIAA, a network of over 5,000 insurance agencies across the US, who by joining together have increased their strength and stability...

Comprehensive auto insurance is an excellent option for individuals who are purchasing new vehicles, as well as for those who cannot afford to replace their vehicle if it is lost to collision, theft, or natural disaster. Residents of Fisherville, KY and surrounding areas who are interested in learning about their comprehensive insurance options can consult a TruePoint Insurance agent to learn if this coverage is the right option for them.

Comprehensive auto insurance covers losses aside from simple collisions, typically including theft, fire, natural disaster, civil unrest and rioting, and the vehicle colliding with an animal such as a deer. If you live in an area where you may experience one of these situations, it may be wise to consider adding comprehensive auto insurance to your package. This will help ensure that you’re fully protected if an unfortunate event occurs.

If you’re purchasing a new vehicle, it’s often common for the lender to require that you carry comprehensive auto insurance due to the value of the vehicle. This helps protect both you and the lender in case of an accident or theft. You may find that you feel more secure, overall, when you carry this type of auto insurance no matter the age of your vehicle. Comprehensive coverage helps ensure that you’re protected no matter what happens, making sure that you can pay to have your car or truck repaired or even replaced as necessary.

When you’re deciding what type of automobile insurance to carry, there are numerous decisions to be made. Consult a friendly representative at TruePoint Insurance to learn more about the best type of coverage for your specific situation. We proudly serve the Fisherville, KY area and are happy to speak with you about the insurance coverage that’s best for you and your family, depending on the vehicles you have and the situations that you frequently find yourselves in.

Condo owners who live in Fisherville, KY may be at a loss of what to do if a neighbor causes damage to their personal property or condo. The agents of TruePoint Insurance can help navigate the process. Owning a condo is similar to owning a traditional home, with one exception. Condos are connected much like apartments. This means the negligence of a neighbor can result in property damage to your condo.

Registering a Complaint

If your condo or personal possessions are damaged due to a neighbor’s neglect, you will need to file a complaint with the property owner where your condo is located. It will be up to them to determine who caused the damage and who will eventually be held responsible for paying for any repairs that need to be made. Your insurance agent will work with the property owner to determine when repairs can be made.

Covering the Damage

In many cases, your insurance company will pay for the repairs to be made so that your condo can be returned to its original state as soon as possible. Both insurance companies will work together to ensure that the responsible party is held accountable for the damages that were caused. This is also true for accidents involving any type of injury that is caused by a neighbor or the primary property owner.

Fisherville, KY condo owners don’t have to stress over their insurance needs. By calling the agents at TruePoint Insurance, they can get all of their important questions answered. The agents understand the frustration of condo ownership, especially when it comes to certain types of risk. Call today to speak to an agent and get the answers you need.

For those that live in the Fisherville, KY area, owning a motor home can be a great option. When you have a motor home, you are going to have a vehicle that will allow you to drive around and tour the rest of the country. At the same time, it will also give you a place where you can relax and sleep when not on the road. If you are going to get a motor home, it is important that you get the proper insurance. There are several situations when someone should get insurance coverage for their motor home.

When Looking for Proper Coverage

One of the situations when someone shoudl get motor home insurance is when they want proper coverage for their asset. A motor home is a unique asset in that it is a combination of a home and a vehicle. Due to this, you need to have insurance coverage that reflects this. With a motor home insurance policy, you can receive the insurance coverage that you need.

When Taking out a Loan

You will also need to get motor home insurance if you take out a loan to buy the asset. A motor home can be very expensive to buy and using a loan makes sense for many people. If you do take out a loan, it is important to comply with the lender’s insurance requirements.

If you are looking to get insurance for your asset in the Fisherville KY area you should reach out to the team at TruePoint Insurance. When you do speak with the team at TruePoint Insurance, you are going to learn a lot more about how you can protect your motor home with an insurance policy. They can then help you get into a proper policy that meets your needs.

Strong listening, oral, and written communication skills

Goal oriented, highly motivated, and resourceful to achieve results

Ability to pay close attention to detail and accuracy

Ability to create and maintain business relationships with prospects and policyholders

Proven track record of trustworthiness, dependability, and ethical behavior

Fundamental understanding of office technology used by small business

Experience and Education:

Customer Service Experience (prior experience preferred)

Knowledge of Personal Lines, Life Insurance, and/or Commercial Lines products (preferred)

Property and Casualty license a plus

High School Diploma or GED

Associates or Bachelor’s Degree (preferred)

Job Related Training/Licensing:

Must have the ability to obtain a Property and Casualty license within the first year of hire.

Responsibilities:

Provide service to the public and policyholders in a pleasant and courteous manner

Be able to communicate clearly and professionally

Prepare forms and endorsements when required

Perform Billing and Customer Service duties in a timely and efficient manner

Meet customer service goals and assist with marketing goals

Be able to successfully navigate our Agency Management System and Carrier Websites

Perform other related duties as assigned

Pay and Benefits:

Salary will be based on experience, with the ability to advance based on performance and license. There will be an initial 90-day evaluation period to determine compatibility, salary increases, and bonus options. Interested Candidates should send a resume to New job Candidate Pooler GA.

There are many advantages to renting a home in Fisherville, KY as opposed to buying. You have greater freedom to move when you want and less financial responsibility. You also have the benefit of purchasing renters insurance to protect your valuables. Renters coverage is practical, affordable, and flexible, making it a smart investment in protecting your assets. Here’s how a renters policy from TruePoint Insurance can work for you.

Protection for Personal Belongings

Whether you’re renting a house, apartment or condo, chances are your landlord will have insurance to protect his property. His coverage, however, doesn’t include your belongings. By purchasing a renters policy, you can get the insurance protection you need.

Renters insurance offers various types of protection to protect you from financial loss. Property coverage protects your belongings. If your rental home is broken into and valuables stolen, property coverage helps cover their replacement cost. It also covers your goods if they’re damaged by vandalism, fire, water due to leaky pipes and other disasters.

Protection against Liability Claims

As a renter, you’re responsible for accidents that occur on your rental property. If someone gets injured while visiting your Fisherville, KY home, you could be held liable for his medical costs. Liability insurance covers accidental injuries to protect your personal funds. It also covers accidental damage to visitors’ personal property.

Protection against Loss of Use

If your rental home is damaged by fire, tropical storm, or other disaster and you have to live somewhere else temporarily while the house, condo or apartment is being repaired, loss of use coverage helps cover these extra costs. This includes hotel bills, restaurant bills, transport bills, etc.

These are just a few ways renters insurance in Fisherville, KY can work for you. To purchase a renters policy, call or visit TruePoint Insurance today.

An Rv is not just a luxury vehicle, but a home on wheels. During your tours in Fisherville, KY, many things can happen, including a road accident. Have you figured out how much loss that would be if you didn’t have any form of insurance?

Well, Rvs are pretty expensive. On top of that, they carry your valuables just like home. Speaking to an insurance expert in TruePoint Insurance can be a great idea as we will help you find out how much coverage is adequate for you.

Why do you need RV insurance?

We have already mentioned that RVs are like our homes on wheels, which means they carry a lot of value on the roads as well as when packed. While many states do not require drivers to have RV insurance, it makes sense to have a substantial amount of coverage in case anything happens to you out there. While they require ordinary driving skills, Rvs are bigger cars. You will need to make accurate estimations when driving or packing.

Factors that impact Rv insurance premiums

While insurance rates are different for every Rv owner, insurance companies use various criteria to calculate based on the information that you provide. Providing truthful information is a requirement as failure to do so can result in fines. Your Rv insurance premiums will be calculated based on the following factors:

The size of your RV

The age of the RV

Whether you are living in it or not

How long you will be using your Rv

Where you pack or store your Rv when not in use

Your location/address and many more

Your RV is a huge investment that needs to be protected at all costs. Large vehicles can cause significant damages and injuries to the parties involved. You don’t want to risk taking a tour in an uncovered car.

Do you need help buying Rv insurance? TruePoint Insurance can arm you with the right information to help you make a wise decision. Visit us at Fisherville, KY today.

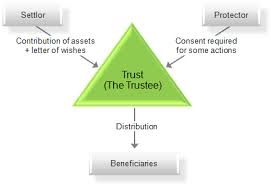

Homeowner and other policies that protect private residences have, for most of their history, been written assuming that the property owner is an individual or married couple. Policies traditionally defined an “insured” or covered person as an individual, married couple or spouse of the individual listed on the policy. However such policies had to respond to a, formerly, rare form of home ownership….trusts.

Besides use as a residence, a home is also often a primary financial asset. As property owners become more sensitive and savvy in handling their finances, the use of trusts to pass on property has expanded. A trust refers to any asset that is controlled or owned by an artificial entity, the trust agreement. Typically, the property owner becomes the trustee, having rights to use the home as a residence, but the legal ownership resides in the trust. The trust allows for tangible property to be passed along to heirs with much more for favorable tax treatment. However, there are consequences that affect insurance coverage and which should not be ignored.

If your home or personal property (furniture, furnishings, etc.) have been transferred into a trust, it is important to share this information with your insurance agent. Then you both may take steps to make sure that the insurance needs of both the trust and the property-users are covered. It is particularly important that liability protection remains intact.

Depending upon the insurer, your homeowner, auto and umbrella policies may have to be modified so that the trust arrangement is specifically recognized and is protected by the policies. It may be that the policy wording already handles things by including trusts or trustees within the meaning of “insured.” In other instances, endorsements may have to be added to include the proper additional insurable interest so that property and liability coverage expands to protect the property held in trust and the trustees.

The existence of a trust means you need to get an insurance professional involved to make sure you can still trust the protection of your various insurance policies.

COPYRIGHT: Insurance Publishing Plus, Inc. 2016+6

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

Insurance is not a product, nor is it a service. Insurance is a promise, a contractual promise that should be entered into with trusted parties.

Insurance policies involve trust. Insurance policies are written agreements that involve at least two parties. One is the insurance company that provides the applicable form of protection. The other is the party who is protected by the policy. These two parties have a contractual relationship with each other. The insurer agrees to protect the insured if the insured agrees to pay for the protection.

The trusting relationship begins before any policy is issued. Insurers want to provide policies to persons who meet their qualifications. Qualified persons are discovered by using applications. Besides collecting identifying information, applications also gather details that determine if a person is eligible for a given policy. The information also helps the insurer decide how much to charge for the coverage, what level of coverage it should agree to grant and the conditions for providing the protection.

The insured should also to be able to trust the insurer. He, she (or a business entity) has to rely on the company actually issuing the type of coverage it promises. The insured also trusts the company to pay for a loss (that is eligible under the coverage) and to handle any loss fairly and efficiently. Both parties must approach the contractual agreement honestly and fairly. The contract is affected if either party fails to act in good faith.

Do you know the details of your insurance policy? Who does?

When an insurance company refuses to cover an eligible loss without a valid reason or when an insured refuses to pay for the policy; these are instances of breaking the contract. An insured may also break the contract if he or she either withheld information or intentionally supplied false information. Of course the information must involve some significant item that would have affected the company’s decision to accept the insured. Breaching a contract may allow an insured to sue a company for coverage or allow a company to void the policy it issued.

Whenever policies are not handled in good faith, there are consequences that impact more than just the two parties. Third parties, such as other businesses or persons, may also be harmed by insurance contracts that turn out to be invalid. Modern economies depend upon the role played by insurance contracts. It would be impossible to handle large transactions without a way to protect all parties against possible losses. Further, many parties would not even attempt certain types of transactions without the support of insurance, such as large building projects, major equipment sales, vehicle rentals and numerous other transactions.

Certainly there are many times when one party fails to handle their insurance obligations in good faith. However, such instances are the exception. Our economy and standard of living are made possible because most parties deal with each other honestly and we all benefit when that happens.

COPYRIGHT: Insurance Publishing Plus, Inc. 2016

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

Many of us avoid or delay decision making. Especially if we are dealing with a new set of issues. Decision making can be extremely stressful.

It’s not surprising that first-time parents report elevated levels of stress and anxiety. In a relatively brief time period they will be expected to make a large number of often critical decesions.

Before you can take your newborn home you will have to decide which Child Safety Seat is right for your situation. The car seat is vital for your child’s safety! The child’s car seat comes down to your judgment and perceived importance of seat safety options, the seat integration to your vehicle, budget, and other factors relating to what best fits your family. Safety is obviously paramount, but you also have to consider Georgia Car Seat Laws. These laws have been designed with your child’s safety in mind and should provide valuable insights. Make sure you’re up to date with the car seat laws in your state and review your vehicle manual for proper fitting.

According to Georgia Consumer Protection: The 4 Steps for kids car seats are: 1. Rear-Facing Infant Seats in the back seat from birth to at least one year old and at least 20 pounds. 2. Forward-Facing Toddler Seats in the back seat from age one to about age four and 20 to 40 pounds. 3. Booster Seats in the back seat from about age four and 40 pounds to at least age eight, unless 4’9”. 4. Safety Belts at age eight or older, or taller than 4’9”. All children age 12 and under should ride in the back seat.

According to www.safety.com: (Updated April 16, 2020)

Bringing Home Your Newborn? You should consider the Britax B-Safe Infant Car Seat.

Want a Child Car Seat that adapts to the changing needs? Look into the Graco 4Ever DLX 4-1 Infant to Toddler Car Seat. This seat can be used in any of the four different positions.

Still, driving a small car? There’s a child safety seat for you. The Graco SlimFit 3-1 Convertible Car Seat is for those parents still fight to keep the choice of vehicle. Wait there’s more the SlimFit 3-1 is another Child Car Seat designed to adapt with your child growth. This seat has been designed for children between 5 and 100 pounds.

A Child Passenger Safety Technician can show you how to install or inspected this critical addition to your auto.

Need help installing your Child Safety Seat? Maybe you need the comfort of a second opinion. Regradless, the organizations listed below have provided a helping hand for new parents in the past. You may want to make a quick call beforehand. Below is a list of places you can call and schedule an appointment to have a Child Passenger Safety Technician show you how to install your car seat or have it inspected.

I hate this seat belt. I can never get it fastened.

Auto Dealers don’t have a big enough basement when a storm is bearing down.

What is a Dealer’s Blanket? It has nothing to do with auto dealer giveaways. The Dealer’s Blanket is a form of business insurance that provides physical damage coverage for Auto Dealers. You may have heard it referred to as Open Lot Insurance or Dealers Open Lot Insurance. Regardless of the name, this policy is essential protection for many car lots.

Consider your own car insurance. In many ways, the Dealer’s Blanket looks similar to your personal auto policy. The primary purpose of the policy is to provide protection against dealer loss. Specifically, losses resulting from comprehensive and collision protection. While there are many similarities, there are also some significant differences.

Personal Auto policies provide liability coverages. Liability coverage is not the purpose of the Dealer’s Blanket. It is a coverage that they have access to, but it is not provided by the Dealer’s Blanket. Liability protection for auto dealers is provided by the Garage Liability Policy.

Insurance companies require Georgia individuals to provide identification to insure their autos. We refer to this identification as a VIN or vehicle identification number. This serves two main purposes. First, it gives insurers a nearly fail-proof input for pricing their exposure as it relates to your specific vehicle.

While the VIN provides accurate information related to the vehicle’s replacement cost. What it fails to do is provide insights into the present condition of your vehicle. To address this shortcoming, you may even go as far as require you to provide a current photo of your car.

Individuals insure against comprehensive and collision risk. For the most, new and used car dealerships insure against the same. What differences exist?

Auto Dealer insurance specialist in the Low Country and Georgia’s Coastal Empire

Auto Dealers in Georgia and other states use the Dealer’s Blanket to transfer comp and collision risks. What is the Dealer Blanket and why auto dealers need them?

Individuals are likely to have the same vehicle all year. Most will own vehicles for many years, some several decades. Used and new auto dealers can’t stay in business by holding on to cars for years or decades.

Successful auto dealerships turn their inventory several times each year. The average US Car Dealer’s inventory turnover is more than 13 times. A dealer with an average inventory of 50 cars would have 650 policy endorsements each year. Those policy changes would be required just to keep up with the new inventory vehicles. To avoid overpaying, they would also need 650 approvals to remove sold vehicles. That would present a serious problem! Making over four insurance transactions every business day seems inefficient. Creating issuers for both the dealer and the insurance company. With so many transactions, it’s also possible the process may put the dealership at risk. Failing to record just one transaction could end in a multimillion-dollar loss. Not a claim! Failure to record a newly purchased vehicle is a problem. the sale was never recorded on the books of the insurance company, the auto lot will be on the hook financially. How many Georgia auto dealers do you know that could serve such a substantial loss.

Let’s give the insurance companies some credit. Recording real-time vehicle information was throughout the policy year doesn’t work. With that said, how do Insurance companies keep track of Georgia Auto Dealer risk?

How to Auto dealers address comp and collision risk.?

Comp and collision is priced and transferred via the Dealer’s Blanket. How it’s done varies between insurance companies and between dealers. If you’re a Georgia car lot, you must understand how your risk and premiums are calculated. The insurance company can not be expected to know how your business changes. Often, the difference between good and bad insurance boils down to communications. Having a good a local Georgia insurance agent can go along way. This thought is easy If your one of those people that respect the value of local contacts.

Insurance markets can not totally eliminate risk. The only way to totally eliminate risk is to avoid it. For those in the business of selling vehicles, this is not an appealing option. The Dealer’s Blanket is a great way to transfer risk. But, it is critical that all parties are on the same page. Problems are largely dependant on establishing the necessary communication process. A critial first step is understanding the Dealer’s Blanket. Combined with accurately communicating auto inventories, car deals can significantly reduce financial exposures.

WARNING: Accurate Inventory Critical

Auto Dealers can easily protect their inventory. Calculating the required coverage can be sticky at times. Photo Credit attribution 1

There are two primary approaches to calculating dealer open lot premium:

Non-Reporting Forms – This method is most often used by smaller used car dealers. Georgia Car lots with inventories of $100,000 or less will in most cases use the Non-Reporting method. This may not necessarily be by their choice. Often the cost associated with the monthly reporting eliminates dealers with smaller inventories.

At the beginning of each policy period, the dealer must declare a coverage amount. CAUTION REQUIRED! When a loss occurs, and a claim is submitted, the insurance company will most likely review and calculate the dealer’s inventory. If it is higher than the declared amount, THERE COULD BE A PROBLEM. The underreporting will likely trigger the coinsurance clause. As a result, the dealership will bear the financial responsibility for the difference.

Monthly Reporting Form – This method requires the dealer to periodically update the insurance carrier. This forces dealers to take on additional work, but this method is cost-effective. It always reduces concerns associated with paying coinsurance.

The Dealer’s Blanket is important. But there are many additional coverages that Georgia Dealerships should consider. Some of the most common insurance coverages for Auto Dealers include:

Commercial Property

Business Personal Property

Workers Comp

Business Income

Garage Liability

Garagekeepers

EPLI

Business Income

and Cyber Liability.

We mentioned GarageKeepers, which is another coverage that is specific to the Auto Industry. This coverage protects vehicles of customers that have been left in your care. Dealers that also offer repair work will most likely need to add this coverage too.

Attribution 2.0 Generic (CC BY 2.0) Photo by John Lloyd, taken on October 22, 2009, distributed by Flickr

Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get Directions