TruePoint Insurance is one of Georgia�s fastest growing insurance agencies. We are affiliated with SIAA, a network of over 5,000 insurance agencies across the US, who by joining together have increased their strength and stability...

Knowing how to pick out the correct car seat for your child is vital for your child’s safety! When picking out your child’s car seat it comes down to your personal preference, budget, and what best fits your family. Make sure you’re up to date with the car seat laws in your state and review your vehicle manual for proper fitting.

According to Kentuckystatepolice.org: The 4 Steps for kids are: 1. Rear-Facing Infant Seats in the back seat from birth to at least one year old and at least 20 pounds. 2. Forward-Facing Toddler Seats in the back seat from age one to about age four and 20 to 40 pounds. 3. Booster Seats in the back seat from about age four and 40 pounds to at least age eight, unless 4’9”. 4. Safety Belts at age eight or older, or taller than 4’9”. All children age 12 and under should ride in the back seat.

2020’s Top Rated Car Seats:

According to www.safety.com: (Updated April 16, 2020) • The best car seat for growth of your child is: Graco 4Ever DLX 4-1 Infant to Toddler Car Seat. • The best infant car seat is: Britax B-Safe Infant Car Seat. • The best car seat for smaller vehicles: Graco SlimFit 3-1 Convertible Car Seat.

Below is a list of places you can call and schedule an appointment to have a Child Passenger Safety Technician show you how to install your car seat or have it inspected.

I hate this seat belt. I can never get it fastened.

2. Norton Children’s Hospital: https://www.safekids.org/inspection-stations#KY Address: 315 E Broadway Louisville, KY 40202

3. Norton Children’s Medical Associates-Shelbyville https://www.safekids.org/inspection-stations#KY Address: 150 Frankfort Road Shelbyville, KY 40065

4. Norton Children’s Medical Center- Brownsboro https://www.safekids.org/inspection-stations#KY Address: 4910 Chamberlain Lane Louisville, KY 40241

5. Norton Women’s & Children’s Hospital https://www.safekids.org/inspection-stations#KY Address: 4400 Dutchman’s Lane Louisville, KY 40207

6. Kentucky State Police (kentuckystatepolice.org) KSP advises all troopers at all 16 posts have been trained as certified safety seat technicians

7. UK Health Care The Safe Kids Car Seat Inspection Station at Immanuel Baptist Church (ukhealthcare.uky.edu) Address: 3100 Tates Creek Road Lexington, KY 40502

A variety of businesses

are routinely operated in homes. This article discusses aspects of particular

operations. Refer to Home Businesses – Basics for background information

on coverage as well as our other articles discussing different in-home businesses.

Daycare or In-Home

Schools

Coverage for abuse or

sexual assault for small schools is often difficult to obtain at a reasonable

price. Limited corporal punishment coverage for teachers who are employed by a

school system may be available from your homeowners carrier.

If you are an independent tutor or run your own school, most homeowners

policies cannot be modified to include corporal punishment. Abuse and corporal

punishment may be available through the association(s) that

specializes in your type of school.

While the company that

writes your HO policy may be willing to add an endorsement to cover piano

lessons, most will not want to cover a three-to-five child daycare operation.

Liability coverage may be purchased separately. Coverage for property and

liability can be provided through a Businessowners policy,

but none of these forms includes professional liability or abuse or corporal

punishment.

Does your homeowners insurance cover a small daycare?

Specialty schools, such

as ballet, sports, personal training, animal training, or horseback riding will

require specialty coverage. Again, your trade organization, or independent

agent can often find you coverage at a reasonable price.

Workers compensation is

essential for any person you employ.

Driving students in

private vehicles or bus-like vehicles poses special problems. You must hold a

Commercial Driver’s license if you haul more than 16 people including the

driver. Your school is probably too small to qualify for standard business auto

insurance. If standard coverage is unavailable, many states have assigned risk

pools and other mechanisms to provide you coverage-sometimes at reasonable

prices. A good independent agent will understand these markets.

Your state will also

have laws regulating the transportation of students and these laws may require

a special license when transporting fewer than 16 people. Subcontracting the

driving does not lessen your responsibility for a whole raft of laws from

vehicle accidents, workers compensation, ADA, and whether the driver has met

the new substance abuse requirements.

COPYRIGHT: Insurance Publishing Plus, Inc. 2016

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

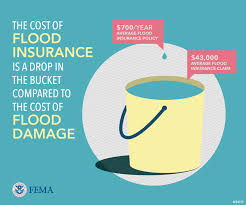

Learn about flood insurance before the waters start to rise.

Anyone that lives in the Fisherville, KY area needs to carefully consider their home insurance needs. One form of insurance that should be considered is flood insurance, which will provide specific coverage if your home is damaged by a local flood. There are several situations when someone should get flood insurance on their property in this area of Kentucky

Anyone with Lender Requirement

Does your home mortgage require flood insurance?

The first situation when someone in Kentucky should get a flood insurance policy is if they are required to have it by their lender. Mortgage lenders are aware of how serious flood damage can be. Due to this risk, lenders often require borrowers to carry flood insurance if they are in a flood zone. Depending on what flood zone you are in, the lender could require you to escrow payments monthly to ensure coverage.

Needs to Cover Against Risk

Flood Loss versus Cost. You do the math!

Even if there is a small risk for flood damage in your area, you should still consider getting flood insurance. If you do not have a mortgage or are not required to carry it, you should still carefully assess your risks and current insurance coverage. If you are near a waterway that could flood, you should consider getting an additional flood insurance policy to ensure you are fully covered at all times.

When you are looking to learn more about flood insurance in the Fisherville, KY area, you should speak with the team at TruePoint Insurance. Choosing a flood insurance policy can seem quite complicated and challenging. When you call TruePoint Insurance, the team of insurance professionals will be able to provide you with a full assessment to help you determine what type of insurance is right for you. They can then help you get into a policy that provides adequate coverage.

As you approach your golden years, you may find that your plan to provide for your dependents isn’t as solid as you’d like. In these cases, a customized life insurance strategy from TruePoint Insurance can help you create a better future for those you may leave behind. While age is an important factor, older residents in the Fisherville, KY area still have life insurance options that can build a stronger foundation for their dependents.

Be Realistic

Your age isn’t the only factor agents look at when considering life insurance coverage. Your agent will also look at your:

History of tobacco use

Gender

Health history

High-risk lifestyle activities

Driving record

Senior citizens with the right combination of factors can still find affordable and adequate life insurance coverage. Your insurance agent can help you understand how these factors affect your current options.

Try a Term Policy

Term life policies are contracts that provide coverage for a short period of time. The coverage period can be anywhere from a few months to several years. These contracts come with very specific coverage requirements. Your insurance agent can help you create a contract that covers your most likely scenarios to ensure your dependents receive full payment.

Bulk Up Existing Policies

Your existing life insurance coverage may not be enough to cover current circumstances. In that case, your insurance company may be willing to work with you to expand coverage.

Think About Survivorship Insurance

Survivorship life insurance is a highly flexible option for married couples with dependents. The shared risk generally decreases premiums and maximizes potential benefits. These contracts are designed to pay out when the last covered subscriber passes away.

Find the Best Strategy for Your Family’s Financial Future

TruePoint Insurance agents can help you find the life insurance coverage you need for your family’s future. We offer customized policies for residents in the Fisherville, KY area. Call us to talk about your life insurance options.

When’s the last time you consider the impact of a street or highway intersection? For us, it was on our first trip to Savannah, Georgia.

Intersections should

be designed with driver and passenger safety in mind. However, In the US,

roughly 2.5 million auto accidents occur in intersections each year. That’s 10%

of the 250 million vehicles in the US.

Solving the

intersection dilemma in a roundabout way

The Dilemma: Intersection or Roundabout

For decades Americans have had a fancy for

cars imported from Europe. US consumers have found numerous reasons to support

their purchase of imported autos. Arguments included performance, economy,

style, and a plethora of other advantages. But the most frequent and compelling

has been safety.

In recent decades America has been importing

another vehicle for auto safety. This time, it’s not automobiles, and it is

considerably less popular with American drivers. Roundabouts, an alternative to

intersections, have long been popular in Europe. Also known as traffic circles,

rotaries, or road circles, they replace intersections.

Turning Left is Dangerous to Your Health

Roundabouts have been slow to catch on in America. Why? I’ve seen some reasons, none of which make sense. What does makes sense are traffic circles:

Speed Slower speeds reduce damage and fatalities

Eliminates Left Turn Why does UPS give drivers routes designed to avoid turning left? Because it reduces accidents and delays.

Energy Efficient Braking to a full stop waste fuel. Starting from a dead stop is even more inefficient.

Trigonometry Eliminates many of the more dangerous angles in which a car can be struck.

Safety Most important, roundabouts lead to improved safety.

The Institute for Highway Safety reports that roundabouts reduce crashes involving injury by 75%. Even more amazing the study reports collisions with fatalities are reduced by 90%.

Coming full circle on street and highway intersections

Why isn’t your insurance agent talking about

roundabouts?

There may be a good reason, but I can’t think

of a single one at the moment.

Insurance agents sell products that indemnify the insured in the event of a loss. Good insurance agents work with prospects and customers to help identify risk. They then provide input and access to effective solutions.

By raising awareness of the safety benefits of

traffic roundabouts, we at TruePoint Insurance believe that we are doing our

part to reduce risk. We’re arming our clients and prospects with the data that

supports traffic circle safety.

Compared to the intersections commonly used in

America, Roundabouts significantly reduce risk. The 37% reduction in overall

collisions may pale in comparison to the 75% reduction in injury collisions.

And while both fall short of a 90% reduction in fatality collisions, this is

still jaw-dropping data.

The agents of TruePoint Insurance encourage

each of you to take a stand. Raising awareness is the path to safer streets and

roads. Saving lives by performing an action that will save money on insurance.

Roundabouts significantly reduce risk when

compared to the intersections used today. The 37% reduction in overall

collisions may pale in comparison to the 75% reduction in injury collisions.

And while both fall short of a 90% reduction in fatality collisions, this is

still jaw-dropping data.

The agents of TruePoint Insurance encourage each of you to take a stand. Raising awareness is the path to safer streets and roads. Saving lives by performing an action that will save money on insurance.

A variety of businesses

are routinely operated in homes. This article discusses aspects of particular

operations. Refer to Home Businesses – Basics for background information

on coverage as well as our other articles discussing different in-home

businesses.

Today’s Landlords are held responsible for their actions

Landlord

The homeowners policy is

designed to cover landlord-occupied residential buildings, landlord-owned

personal property, and loss of rents (after a fire or other covered cause of

loss), premises liability and medical payments. Note that the maximum occupancy

that may be covered under an HO policy is a four-family dwelling. A

dwelling policy may be used for 1-4 family structures that are not also

occupied by the landlord.

For landlords with

residential property containing from five to sixty units,

a Businessowners policy (BOP) is usually appropriate. It insures

buildings, landlord personal property, loss of rents (after a fire or

other covered cause of loss), premises liability and medical payments.

Most Bed and Breakfasts

do not qualify for coverage either in the homeowners or dwelling insurance

program. Bed and Breakfasts will require a combination of tenants coverage for

the resident owner/manager, and a BOP to cover buildings, landlord owned

personal property in boarders’ rooms, loss of business income (rents and fees)

and the extra expense to operate (after a fire or other covered cause of loss),

premises liability and medical payments.

Contracts often drive rental insurance policies

For landlords who have

office or retail tenants, the BOP provides broad coverages for

buildings, landlord personal property, loss of rents (after a fire or other

covered cause of loss), premises liability and medical payments.

Worker compensation is necessary for any employee. Talk with your agent. Most states require workers compensation for resident managers even if you provide only free lodging as payment. Make sure you have certificates of insurance for any subcontractors (painters, plumbers, etc.) you hire to do work for you. If the subcontractor has no insurance, you may be responsible for the subcontractor’s work-related injuries.

COPYRIGHT: Insurance Publishing Plus, Inc. 2016

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

Boating season can bring out the best in Kentucky residents, especially those residing around Fisherville, KY. At TruePoint Insurance, we understand the water life and enjoy it with our clients. While we all enjoy days and afternoons out on the water, we also want you to remember three tips to stay safe while out on the water.

Keep Your Life Jacket On

It is not uncommon to travel the Kentucky waters and catch boaters riding without their life jackets. In the event of an accident, the riders could potentially be thrown from the boat. With a life jacket, they will surface to the water and be able to breathe while getting to safety.

Keep the Crowding Minimal

Each boat comes with a weight limit and a capacity amount based upon its size. A common issue that happens with boaters in Kentucky is overloading the boat with either people, supplies, or both, causing it to flip from the stress it is under. If you are planning to use your boat for fishing and hauling equipment, make sure sure that you do not carry too many people out with you.

Leave the Alcohol Onshore

While you are operating your boat, you should not be drinking. The pressure and influence to drink while operating the boat are limited if it never comes onto the boat with your passengers. Leave the alcohol onshore and stock your boat instead with fresh bottled water and sports drinks to keep everyone hydrated while enjoying the water.

Top it Off with Boat Insurance

One of the best ways to secure your boat, however, is to have boat insurance should you find yourself in an accident while out on the water. If you live in the vicinity of Fisherville, KY, call our agents at TruePoint Insurance for more information on our policy offerings.

Businesses price their products to cover the costs of production as well as their labor, sales marketing, and other major expenses. Prices also reflect some post-sales costs such as handling repairs or replacements under warranty. At one time many industries used a pricing strategy for their products that failed to reflect their true costs. A once-popular assumption was that lower prices would promote increased sales and the higher sales volume would make up the cost difference. The strategy wasn’t successful. It hasn’t worked for the auto industry, the computer industry or the insurance industry.

The problems of the

insurance industry became apparent within the turn of the century and were

drastically exasperated by several natural and financial catastrophes. Events

such as terrorist attacks, hurricanes, housing market and banking meltdowns all

substantially affected the insurance industry. The insurance industry’s

attempts to gradually correct their pricing had to be sped up; substantially!

Why are insurance premiums so high?

For much of the 21st

Century, insurance companies have had to handle many more claims being

presented many years after their policies have expired. In the case of

pollution, asbestos and employment practices; the industry is being asked to

handle losses that policies weren’t designed to even cover.

Well, what can a

business owner do to minimize their high insurance cost? Before considering

sacrificing the amount of protection a business carries just to save money,

consider alternatives. Some other solutions would be:

1. Review your coverage:

a. Take a close look at your insurance. Could you increase the

deductibles to lower your premium?

b. Are you carrying physical damage coverage on commercial

vehicles that aren’t worth it?

c. Are you insuring items you could replace out of pocket? Are

there pieces of equipment that are insured when they could be replaced from

operating funds without submitting a claim?

2. Review your exposures:

a. Could you reduce the premium by installing an alarm system or

fire protection system? Would these premium savings offset the cost of the

system?

b. Could you implement safety programs that would reduce the cost

or make the insurance company more interested in providing coverage? For

example: driver safety programs, back to work programs, safety training in

proper use of equipment and job functions.

3. Identify your insurance goals:

a. Do you need an insurance company that can provide loss control

services?

b. Do you need an insurance company that can provide claim-handling

services for your Workers Compensation insurance?

c. Do you need an insurance company that will allow you to make

payments by phone or on-line 24/7?

Shopping and price are

not the only issues in insurance. What you don’t know can cost you more in the

long run than you could ever save in premiums. Discuss your situation with an

insurance professional and make the choice that works for you.

COPYRIGHT: Insurance Publishing Plus, Inc. 2016

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

If you own and/or run a smaller business, your insurance needs may be properly handled by a business owners policy (BOP). A BOP is a single form that offers both property and liability protection. Retailers, wholesalers, small contractors, artisan contractors, dry cleaners, restaurants, offices and convenience stores (including those with gas pumps) are eligible for BOP coverage. All such operations may be insured by a BOP as long as they do not exceed the square foot or annual sales limits established for the program. Cooking operations, due to the higher fire and other accident exposures, have significantly more restrictive guidelines.

Property Coverage – BOPs protect buildings as well as the following:

The policy’s protection for business personal property (such as

office equipment, copiers, desks, etc.) applies whether the property is located

inside or immediately outside the covered buildings. The category also includes

property you own, lease or control (i.e., borrow or control) as long as the

property is used by the business.

One item of importance, the BOP does NOT provide coverage for loss

of use of damaged or destroyed property, nor for loss created by an actual or

perceived loss in value of goods after a loss takes place.

Liability Coverage – A BOP’s liability coverage provides comprehensive protection for claims or suits made by other parties. Specifically, it covers losses involving injury to other persons or damage to property that belongs to others. It also provides limited protection against personal injury (slander or libel), advertising injury and losses involving an operation’s products or services.

Naturally, there are certain situations that are not covered by a BOP. For instance, there is no coverage for losses involving most vehicles, money, and securities; illegal property (contraband), land, water, growing crops or lawns; or watercraft.

building additions

(completed or being built)

indoor

and outdoor fixtures

Clothes

Dryers

machinery

and equipment

landlord

furnishings,

mowers, ladder, snowblowers, and similar maintenance property

outdoor

furniture

floor

coverings

Refrigerating

appliances

ventilating

appliances

Cooking

appliances

Dishwashing/Drying

appliances

Clothes

washers

materials,

equipment, and supplies

temporary

structures located near the insured premises

Enhancing Coverage – A BOP may be supplemented to provide additional

protection. Property coverage options include adding insurance for accounts

receivable, valuable papers and records, earthquake, spoilage, etc. Liability

coverage can be expanded to handle additional business interests, limited

vehicle liability, losses related to personnel situations, liquor liability and

injuries to leased employees.

A BOP may be the answer to your company’s coverage needs and it may be worthwhile to get more information on the BOP from the nearest insurance professional.

The BOP provides other coverage than the

protection mentioned in part 1. The following protection can be selected under

the BOP.

Optional Coverages

Outdoor Signs–Payment is available for

direct physical loss or damage to outdoor signs at the described premises.

Eligible signs may be owned by the named insured or owned by others but be in

the named insured’s care, custody, or control.

Money and Securities–Coverage applies to loss

of only the named insured’s money and securities used in its business while

that property is at banks or savings institutions, inside the named insured’s

living quarters, inside the living quarters of a partner or employee, at the

described premises or while in transit between the places referenced.

Employee Dishonesty–The

policy

pays for direct loss of business personal property and money and securities due

to dishonest acts its employees commit, whether they act alone or collude with

others to do so.

Equipment Breakdown

Protection Coverage–Coverage is available for loss or damage directly caused by or

that results from electrical failure or mechanical breakdown to covered

property. Covered property is electrical, mechanical, or pressure machinery and

equipment

Liability Coverage – A BOP’s liability coverage provides comprehensive protection for claims or suits made by other parties. Specifically, it covers losses involving injury to other persons or damage to property that belongs to others. It also provides limited protection against personal injury (slander or libel), advertising injury and losses involving an operation’s products or services.

Naturally, there are certain situations that are not covered by a BOP. For instance, there is no coverage for losses involving most vehicles, money, and securities; illegal property (contraband), land, water, growing crops or lawns; or watercraft.

Enhancing Coverage – A BOP may be supplemented to provide additional

protection. Property coverage options include adding insurance for accounts

receivable, valuable papers and records, earthquake, spoilage, etc. Liability

coverage can be expanded to handle additional business interests, limited

vehicle liability, losses related to personnel situations, liquor liability and

injuries to leased employees.

A BOP may be the answer to your company’s coverage needs and it

may be worthwhile to get more information on the BOP from the nearest insurance

professional.

COPYRIGHT: Insurance Publishing Plus, Inc. 2017

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without the written consent of Insurance Publishing Plus, Inc.

Handyman Services Insurance costs for Contractors can vary widely. Insurance companies view roofers as a high risk. In fact, most standard carriers will not even write coverage for roofers. Why? Because they are one of the ten riskiest jobs. On the other end of the scale are jobs like grading of land.

The Jack of all Trades Tinker, Handyman, or Jack of all Trades, regardless of the name you use, the risk is the same. A handyman is an individual that can perform a wide range of jobs. At first blush, it would seem that insurance for a handyman would be considered low risk. That is bad thinking. Insuring a Handyman poses one major problem for insurance companies. What does a handyman do? Work performed is a primary factor in calculating premiums. We know what Roofers do. They install and repair roofs on homes and commercial buildings. A risky endeavor that warrants a higher insurance premium. Occupations that are less risky warrant lower insurance premiums. Such is the case for lawn care providers. Handyman insurance premiums are significantly lower than roofers. They should be, the work they perform is not that risky. Or is it?

Handyman jobs

What does a handyman do? Minor repair, light domestic work, or mechanical jobs are likely responses. Handyman insurance might cost more than one would think because no one knows what they are going to do. In the insurance industry, uncertainly almost always corresponds to higher premiums.

A Handyman might perform low and straightforward risk functions such as:

Changing a light bulb

Window cleaning, or

Cleaning

But it’s more likely that they are performing higher risk jobs:

Carpentry

Gutter Cleaning or Repair

Window installation

But what happens when the handyperson starts playing jobs that require a license? A handyman can quickly alter their risk profile. By performing the following, then we are no longer dealing with a low-risk contractor:

Heat, AC or plumbing installation or repairs

Handicapped or Senior Living Modifications

Electrical work

Home Security Installation or Repair

Foundation repair and installation

Chimney sweep or Fireplace Repair

Some Jack of all Trades will, regularly, perform high-risk jobs. Can a handyman repair a roof?

What happens if, frequently, they start to replace entire roofs?

Could happen?

NO. IT DOES HAPPEN!

Bob The Builder

Bob the Builder or Tim “The Tool Man” Taylor Over the years, Hollywood has created several iconic Handymen and women. But it is the contrast between Bob the Builder and Tim “The Tool Man” Taylor that gets my attention. The performance of these two a generation ago are perfect examples. Both portraying handymen, they demonstrate the dilemma that confronts insurance companies.

Looking for someone with a toolbox full of tools that can fix anything? The animated character, Bob the Builder is your man. For an insurance company, Bob is a great risk. His attitude and skills allow him to complete any job. Doing things the right way means that the risk associated with Bob’s work as a handyman is limited. As a result, he should warrant a low insurance premium.

But there is more to this discussion. The term, Jack of all Trades, is synonyms with Handyman. The original phrase was, “A jack of all trades is a master of none, but often better than a master of one.” The expression is intended as a compliment. The original quote placed value on generalist, those with a broad set of skills.

Jake of all Trades

Over time we have modified the phrase to “a Jack of all Trades, and a Master of none. In these instances, the Jack of all Trades is portrayed as someone skilled in many areas. However, their skill levels are most likely to be inferior. Some of you will remember “Home Improvement,” a 90’s sitcom, starring Tim Allen. Tim portrayed another iconic Handyman; Tim “The Tool Man” Taylor. Every week, Tim Taylor brought humor to American homes. We watched as he managed to once again foul-up another home improvement project.

Risk Management for a Handyman The agents at TruePoint Insurance work with handymen. Our process provides insight into your business. With this information, we can find the appropriate coverages for your Handyman business. We will work with you to craft insurance coverage that addresses your risks. Insurance is just one component of risk management. We will also work to help you to better understand all the risks. We could just sell you an insurance policy. But our goal is to protect your business in the most effective way we can.

The option is yours, the number is ours. Call now and get started.

Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get Directions