TruePoint Insurance is one of Georgia�s fastest growing insurance agencies. We are affiliated with SIAA, a network of over 5,000 insurance agencies across the US, who by joining together have increased their strength and stability...

Many insurance policies have deductibles. A deductible is a set dollar or percentage amount of a claim. The insured is responsible for paying this part before any payments will be released by the insurance company. The purpose of insurance is to reimburse the insured in the event of a loss. Insurance companies pool risks, which work to make payments more affordable for all. Insurance works because it accepts large financial exposures, spread over a geographically diverse group. Most of us have at some point dropped and broken an egg. Did your insurance company replace the broken egg? Insurance, the mechanism that we use to spread risk, fails to work if it is expected to cover all losses. Items below a certain threshold significantly reduce the effectiveness of insurance. Deductibles work to stabilize the insurance process. By reducing the number of small claims, deductibles reduce inefficiencies.

How Insurance Deductible Benefit Consumers

While consumers may find it difficult to accept, deductibles lead to lower premiums. Don’t take my word; you can demonstrate the theory yourself. You most likely have the ability to raise and lower deductibles on your policy. Re-quote your coverage; using both higher and lower deductibles. What you will find is that premiums rise as deductibles decline. You will have proof that the cost of insurance declines with higher deductibles.

How Insurance Deductible Benefit Insurance Companies

Moral Hazard My Great Grandmother used to tell me that locks keep honest people honest. For insurance companies, deductibles can be viewed the same way that my Great-Grandmother saw locks. Example: Ed is trying to sell his boat. The best he can get is $1,200, but he still owes the bank $1,500. Instead of taking a $300 loss he could call his insurance company and reports it as stolen. Then he would have the $1,500 to pay off the boat.No! In this case, the $1,000 deductible removes the incentive to commit insurance fraud. It significantly reduces the chances of a loss for the insurer.

Deductibles reduce exposures to Moral Hazards: Locks keep honest people honest.

Morale Hazard Unlike moral hazards, which are the result of an illegal action, morale hazards are more akin to neglect. Individuals that willing to expose insured property to hazards are considered morale hazards. For example, leaving a cell phone on your front porch isn’t illegal. It could be a perfectly beautiful day or a torrential storm. Would it be illegal if a 4 year old mobile phone was left in a hail storm? No. But this phone is old, and it has an insurance policy. Is it illegal to use the storm as an avenue for a new phone? Probably not. But there are clear ethical issues. This is a moral hazard.

Deductibles reduce exposures to Morale Hazards: Locks keep honest people honest.

Claims Cost: Relative to the size of the loss, insurers pay out a significant amount more on smaller claims. This is due to the considerable impact of fixed cost. Deductibles improve efficiencies: Insurance is intended for catastrophic losses or larger financial exposures. Deductibles occur on most property coverages. The property would be tangibles such as buildings, homes, vehicles and other real property. Until very recently deductibles have almost entirely excluded from liability claims. Giving consumers the option to include deductibles liability coverages is becoming more common. Deductibles are a form of risk retention. They serve as a way to level the playing field for both the insurance company and the insurer. They give insurance companies a tool to reduce fraud and other manipulation. Deductibles also work to enhance the efficiencies of the insurance process. When used responsibly deductibles make it easier for everyone to minimize risk.

Renters Insurance provides personal property coverages for individuals. Also referred to as a tenant’s policy. It protects personal property; excluding buildings, such as homes, dwellings or other structures.

A tenant’s insurance policy is similar in many ways to a Homeowner’s Policy. The most significant difference is that there is no building coverage. The coverages provided by the Renters’ Insurance policy include:

Personal Property coverages often start with a minimum limit of $25,000. But raising this limit to meet the insured’s requirements is seldom a problem.

Liability coverages start around $100,000, with both lower and higher limits available. The coverage provides financial protection to the insured. It protects against accidents causing bodily injury and is a result of actions of the insured. The policy protects not only the insured, but others in the household, and in some cases pets.

Temporary Housing is another benefit provided by this policy. It provides coverage should damage from a covered cause of loss force you to vacate. Included in the renter’s policy is a loss of use benefit which provides tenant’s short term housing in the event of damage to their apartment.

Additional Coverages Available coverages can be added by endorsement that provides unique protection. One of the more common occurrences is when jewelry limits are too low. Increasing the limits on jewelry, or most other collectibles is seldom a problem. The same is true for boats, personal watercraft, ATV’s and many other personal belongs.

What dictates which losses will be covered under a Property and Casualty insurance policy? The Covered Causes of Loss. Obviously, having a clear understanding of what damages will be covered is essential. Covered Causes of Losses are standard list or forms.

The Covered Causes of Loss for all policies comes in one of the three forms listed below:

2. Broad in addition to Causes of Loss covered by the basic form falling objects, the weight of snow, ice or sleet, water leakage from appliances, and collapse from specified causes

3. Special is Also known as the all risk coverage, as this form covers all risk unless they are specifically excluded.

Today most landlords require tenants to have a renter’s policy. If you are confronted with the requirement, don’t view it as an excessive demand. Even though a renters’ insurance policy coverages are similar to a homeowner’s, they are significantly cheaper.

Many insurance companies provide a discount on auto policies to anyone that as a package policy. In most cases, the addition of a renter’s policy creates the package policy. At this point, the cost is insignificant. It is almost as if the insurance company is paying you to buy the renter’s policy. If you have a good insurance and driving history, you should definitely look into a renter’s policy. Even if you don’t give us a call. You never know.

What color is your umbrella? In today’s world, when it comes time to buy insurance, you will find that you have a range of options. The challenge is learning to optimize them to meet your own unique constraints and objectives. Individuals and businesses seeking Kentucky Insurance need to develop a thorough understanding of their insurance options.

Kentucky Insurance Markets:

For decades insurance markets were divided into two categories; Independent and Captive Insurance companies. The independent marketing channel is made up of agents (more accurately, Brokers) that represent multiple insurance companies. Captive carriers utilize agents or employees to distribute their products. This group tends to use more print, television, radio, newspaper and other to generate sales.

In recent years a third market has entered the mix; Direct Carriers. This group has many similarities to the Captive Carriers. The two groups have market plans that look very similar. The Direct Channel takes a much more aggressive approach regards utilizing online resources. The Direct sector of the market not only uses extensive online marketing, but many in this sector also have willingly foregone brick and mortar in favor of online facilities. In many instances, they have shifted the role of the agent to the customer’s computer keyboard.

When it comes to Property and Casualty insurance for

individuals, US Captive Carriers remain the largest player. The market share for Independent Insurance

companies has held fairly steady in recent years, during a time where the

Direct writers are rapidly gaining market share mostly at the expense of the Captive

market.

2017 Personal Lines US Market Share (Auto Insurance, Home Insurance,

and other)

Captive 46.6%

Independent 35.1%

Direct 18.3%

For businesses, the landscape is totally different. Independent Carriers have and continue to dominate this market. It doesn’t seem to difficult, with an 84% market share for US commercial insurance, it seems only logical that all business owners should consider quoting with at least one broker. But why?

Independent agents have access to more markets. More markets should mean better prices and in this case, it certainly does. Business owners are often willing to spend a little more time and put in a little more effort. The point is simple. If their competitor is able to secure insurance at a better value, they will be more competitive. Certainly a position no business owners wants to find himself in!

2017 Commercial Lines US Market Share (Business Insurance)

Captive 16%

Independent 84%

Direct <

1%

Overall the Independent Insurance leads the way, writing nearly 82% more US Property and Casualty insurance than the number two insurance company category, the Captive Carriers.

2017 Combined US Market Share (All Property and Casualty Insurance)

Captive 31.9%

Independent 58.1%

Direct 9.9%

What type of insurance carrier is

right for me?

There is no

right answer for everyone. But if you

are embarking on a search for cheap insurance in Kentucky, you might consider

reviewing the questions below:

Will you be looking Kentucky business

insurance quotes?

As

we noted earlier, Independent Insurance Agents write far more insurance than

the other two types of insurance companies combined. There is a reason this is happening, if you’re

looking for the cheapest insurance chances are you will find it here.

Don’t

just get a commercial insurance quote, while you’re working with your Kentucky

Independent Insurance Agent, have them quote your home and auto insurance. Doing so my end with a lower premium on both

your commercial insurance and your home and car insurance. TAKE ADVANATAGE OF DISCOUNTS EVERY CHANCE YOU

GET.

Business

owners, that don’t get a commercial insurance quote from an Independent Insurance

Agent, are a favorite to pay a higher insurance premium than your

competition.

Do you think the cheapest insurance

is the best insurance?

Price

is important! It’s very important, but

it should never be your only consideration when buying insurance. It doesn’t matter whether you are searching

for household insurance, or for your business.

There are several issues you will want to explore:

Deductibles-Be Extremely cautious if

it is percentage (i.e. 1-2%) instead of a dollar amount (i.e. $1,000)

Causes of Loss

Replacement cost or Actual Cash Value

Standard/Excluded Coverages – Your homeowner’s

insurance policy will exclude many items that you should be given the

opportunity to consider: Earthquake

insurance, sinkhole insurance and many others

Do you understand your business

insurance policy? There are many moving

parts, any of which could spell the end of your business if not properly

addressed.

None

of three insurance marketing venues has a hold on Cheap Insurance. Your personal financial situation, loss

history, age, location along with many other factors will all come into play in

determining your insurance premium.

We

advise our clients to think in terms of the best relative value. Most of us have a job and commute to and from

work four or five times a week. Would you

consider buying a bicycle to provide you transportation to and from your

work?

For

those that live a very short distance from work, this might be a viable

option. For several years I worked

within 2 miles of my home. During this

period, a bicycle would appear to have been a cheap option. I could have saved $10,000, $20,000, even

more had I taken the bicycle route.

That

would certainly be a great relative value if I lived in Gainesville

Florida. But what if I live in

Fairbanks, Alaska, where the average high temperature from November 1st

through March 31st is 10 degrees Fahrenheit? The bike would not be a wise choose.

When

I ask clients to focus on the best relative value, I am asking them to spend a

little more time to review policies. Sometimes

the best insurance policy actual is offered at the lower price or at a premium

that is so competitive that the only logical choice is to pay a little more for

the insurance policy that best fits the client’s needs. Most of us would gladly spend an extra

$20,000 to avoid commuting by bike in Fairbanks, Alaska

Insights

The Commercial Insurance market is extremely dependent

on the Independent Insurance Agency Network.

This group has access to more markets, better options, and overall

better pricing. We highly advise all Kentucky

Business Owners to seek the assistance of an Independent Insurance Agent.

Where can I get lowest cost insurance? Best Relative Value?

Few things are more common than the sight of handmade signs sticking on telephone poles, street signs or mounted on spring and summer lawns that announce nearby yard and garage sales. Succumbing to curiosity or taking a chance on scoring a great buy leads to another familiar scene: a home, with a variety of cars haphazardly parked around it and persons strolling to and from as well as others browsing among the sales items. Generally, the merchandise consists of clothes, baby articles, and toys. Often larger items are for sale such as exercise equipment, furniture, bedding, and appliances. When the event is an occasional one, there are few issues to worry about. But frequency creates important concerns that affect insurance.

Consider someone breaking into your home and making off with hundreds or thousands of dollars’ worth of property. Or how about a fire or storm destroying a home and most of its contents? Usually, there’s no problem since a homeowners policy will handle such losses. However, if a significant amount of the property was stored for sale, that property may either only qualify for limited coverage or may even be ineligible for protection. Property offered at your yard for sale which belongs to others (sold on consignment) is another class of property that may have only limited protection available or, depending on circumstances, might be considered business property and be disqualified from coverage. Example: Joan’s house is broken into the night before her big yard sale. Among the items stolen was a large, expensive set of drums worth nearly $1,000. It belonged to a friend who asked her to put it on display during her sale. Joan’s insurance company denies protection, claiming it was goods for sale and not personal property.

Similar considerations

exist concerning legal liability. For instance, a visitor comes onto your

premises and then fractures a leg and hip when tripping on an exposed tree

root. Because she was old and frail, the injuries require surgery and a long

rehab. The visitor sues you for hospital, surgery and other expenses. Normally

one’s insurance policy would defend you against the lawsuit and, if necessary,

pay any awarded damages. But what if, instead of a friendly visitor, she had

come onto the property to look at items on sale? That could cause a serious

coverage issue.

Determining factors for

either property or liability coverage are how often sales occur and what income

has been made over a period of time (usually the 12 months before the date of a

loss). Depending on those details, the activity involved in the loss could be

considered a business. In such instances, coverage may not exist under a basic homeowners policy.

Yard sales may appear to

be a safe activity, but there are genuine risks to the seller (property owner)

and to the customers who are invited onto the property. It makes sense,

regardless of your insurance situation, to take steps to minimize the chances

of problems occurring.

Safety – property owners bear

responsibility for the safety of their guests. A yard or garage sale represents

an invitation for others to come onto your premises for a financial benefit.

This means that a higher level of watchfulness is due to these legal invitees.

It is important that all reasonable precautions be taken to ensure their safe

use of your premises before, during and after a sale.

Take care in how merchandise is set up and displayed, especially any items that have the potential for causing injury, such as breakables, tools, motorized items.

Clean up any spills immediately, especially any involving broken glass.

Make sure your premises is free of any obvious dangers to customers/shoppers, especially trip hazards.

If you have pets, make sure they are kept away from customers to eliminate any chance for attacks.

Secure access to a covered or shaded area, particularly as a checkout area. On hot days, this can provide a cool down area for sellers and shoppers.

Have access to a fully charged phone to call for assistance in case of emergencies or to arrange for help for food or bathroom breaks.

Limit access to the shopping area by children, both those who are part of the seller’s household and those belonging to shoppers. Sales areas can be hazardous, particularly parts of the yard used for parking cars.

Keep drinking water and spray bottles available to prevent and/or to treat dehydration.

Security – you want to minimize

any chances that you are victimized by using practices that keep persons and

property safe.

Make sure that all doors to your home are locked. If you need easier access to your home during the sale, yourself or another trusted person should be stationed near the door.

Prior to a sale, keep garage doors locked when sales items are stored there.

Set up guards or barriers to discourage any access to your property before or after the sale.

Do not allow shoppers or customers entry to your home, be aware of nearby public places where they can get safe access to restrooms (gas stations, restaurants, etc.).

Take great care in how cash is handled, particularly if you decide to use a cash box. If the latter method is used, be certain that a person is dedicated solely to the checkout area.

For both safety and

security reasons, do not run a yard sale alone. A friend or relative as an

assistant is a must to making sure that customers aren’t endangered and to

reduce chances of theft. Also, never leave the sales area unattended.

If you have yard sales, you should check to see if their frequency and their sales volume create a need for additional protection, such as a form that covers home businesses. An insurance professional is in an ideal position to help you!

COPYRIGHT: Insurance Publishing Plus, Inc. 2015

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

When you buy a home whether it is your first home or forever home, it is a major investment. For most families, it is the largest investment they will ever make. It needs to be protected so that you will always have a roof over your head, a place to call home. If your house is destroyed in a fire or other disaster, you want to be sure that you will be able to rebuild, to replace what you had before it was destroyed.

Before closing on your new home, it is wise to spend time reviewing the home insurance options available to you. TruePoint Insurance in Fisherville, KY can help you understand the different ways that your home can be evaluated.

Market Value

The market value is what your home would have sold for before it was destroyed or damaged. While it sounds like it is a good deal it is a more expensive option because this valuation includes the price of the land that your house is sitting on.

Replacement Cost

Replacement cost is exactly what it sounds like, your policy would replace the house at the current cost to rebuild including labor. The drawback of this type of valuation is that they have a ceiling which is an amount that the value cannot go above. Some policies have what is called an extended replacement cost that can add an additional percentage to what can be collected.

Actual Cash Value

With actual cash value, if your home is destroyed, the age of the damaged items is taken into consideration. If your windows are warranted for 20 years and you have had them for 15 years, you will not get the cost you paid or even what they would cost to replace today, you have used 75 percent of their value so you would receive 25 percent.

If you live in Fisherville, KY you have the experiences agents at TruePoint Insurance to guide you through the type of home insurance policy that is best for you. Stop by their office or give them a call before you make that all important decision.

High school proms are

early chances to participate in a formal event. It is also considered a chance

to act as a full-fledged adult. The event involves arranging a complete evening

of dining, dancing and socialization. However, just as much time should be

devoted to making the event as safe as possible.

It is almost inevitable

that a prom will involve serious exposure to alcohol or other intoxicants. The

evening also involves many young, inexperienced drivers who are excited about

making their way to pre and post prom activities. Sadly, these factors have

combined to make prom season dangerous. Serious traffic accidents often become

the main feature of what should be a night of joy.

Prom-goers and their

parents need to create a strategy for making prom night both memorable and

safe. Here are some tips:

Parents should get all activity details, including dinner and pre and post prom events

Confirm the night’s events with school officials and other parents

Consider arranging a safe, group post-prom activity where participants can be supervised

Clearly lay out your expectations to your son or daughter about acceptable behavior regarding their evening

Discuss all details about transportation, whether they are drivers or passengers

Be sure that communications are set up. If the child does not have a cell phone available, find out the numbers where he or she can be reached during different phases of the evening

If practical, consider arranging for a third party to handle transportation (limo or taxi service)

Consider an amnesty arrangement. In other words, let your child know that they can contact a parent for emergency transportation should something go wrong and, for that evening, they’ll be no lectures or punishments

Help your son or daughter make prom night a bright memory rather than a tragedy. Plan on making safety and fun everyone’s priority.

COPYRIGHT: Insurance Publishing Plus, Inc. 2017 All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

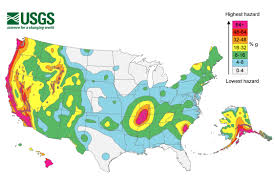

Most homeowners likely

know that, regardless where they live, they may be exposed to a catastrophic

loss such as flooding. It is definitely not restricted to coastal location.

However, the same cannot be said concerning earthquakes. It is much more likely

that only persons living in well-known earthquake areas (such as California and

Alaska) have a high awareness of its danger.

However, the danger of earthquake exists in several large areas of the United States, including a significant part of the Midwest. The New Madrid fault line crosses much of the Midwest, making states such as Indiana, Ohio, Illinois, Ohio, Kentucky Tennessee and Missouri vulnerable to earthquake catastrophe (particularly the latter two states). In the last decade, regular activity has been measured in this Seismic Zone.

A recent development is

affecting this source of loss. Though some questions remain, it appears that

the widespread practice of obtaining natural gas via the process of hydraulic

fracking may be triggering earthquakes in areas that had previously seen little

to no quake activity.

While many persons may

be exposed to the danger of earthquake, only a fraction of such property owners

carry the proper level of insurance. Basic homeowner coverage does NOT include

protection against earthquakes. Without purchasing specific earthquake

insurance, the only protection available for a policyholder is against limited,

consequential damage.

Example: The Johnsons

love their home on the outskirts of Juneau. While they’ve experienced a number

of minor earthquakes, in the few years they’ve owned the home: they did not buy

earthquake coverage. One day a quake occurs and severely damages their home.

The quake breaks a gas pipe and a fire erupts. The fire damage is covered

(though the quake damage is not).

Earthquake coverage is

typically quite affordable. It is generally available for a couple hundred

dollars per year to provide protection for a modest-sized home. While, even in

areas that are in earthquake prone, such losses are low probability; the

potential loss severity is so high that purchasing separate protection makes

sense. So shake up your insurance protection and avoid being totally shaken

down by a disastrous quake!

Insuring yourself against flood risk is a little different than other insurance policies. Many people mistakenly assume that they have flood coverage through their Fisherville, KY homeowners or renters policy, but they don’t. In order to protect yourself from flood risks, you need a specific flood insurance policy to cover related losses. While you can purchase federal flood insurance through an insurance agent, most flood insurance policies are administered through the National Flood Insurance Program (NFIP) and can be purchased by homeowners, businesses, and renters from an insurer who contracts with FEMA.

What Does Federal Flood Insurance Cover?

The maximum flood insurance coverage amount is $100,000 for the contents of your home and $250,000 for damage to the structure. Commercial flood insurance through the NFIP provides up to $500,000 for your building’s materials and $500,000 for damage to the structure. You can also buy what is known as “excess” coverage beyond the limits offered through NFIP through private insurers. Flood insurance coverage for the contents of your home and damage to the structure is sold separately. Coverage for personal property only applies to its cash value basis, whereas buildings are covered for replacement cost.

Federal flood insurance will cover direct physical losses caused by flooding and losses resulting from flooding-related erosion. For flood loss coverage for cars, ask your TruePoint Insurance representative for information about optional flood coverage through the comprehensive portion of your standard automobile insurance policy.

Buying flood insurance

If you have a mortgage and your home is located in an area that has been identified by FEMA as a flood zone, chances are, you have been notified that you need flood insurances. If not consider review the previous link regarding who needs food insurance. If you would like additional information, one of our agents will be more than happy to assist.

When buying flood insurance coverage, remember that almost 100 insurance companies offer NFIP policies. It’s easy to purchase. You can purchase a Federal flood insurance policy directly from an insurance professional. However, it does require a waiting period of 30 days before the policy takes effect.

Flooding can occur at any time and threaten your Fisherville, KY home, so don’t wait until the last minute to purchase it. Call TruePoint Insurance today for more information about protecting yourself from the risks of flooding.

It depends! Finding the best business insurance for many small businesses can be a challenge. Most small business owners in Kentucky will see that they have multiple options. Generally, competition leads to lower prices for canny consumers. With that said, commercial insurance is not a commodity and finding the best value may take a little effor.

Prices paid for Kentucky business owners’ insurance may range widely. Commercial insurance rates in Georgia and South Carolina are no different. Chances are, the more unique your business is, the tougher it will be to find a great deal on commercial insurance. Ferreting through the long list of products makes it difficult.

Insurance Options

To find the best commercial insurance for you, start by reviewing your options. Insurance companies do not write insurance in all states. It’s not uncommon to see a company provide great rates to business in one state, but for some small businesses, you will find that they don’t have a lot of options. Auto dealerships, certain trucking classes, and roofers are good examples. Regardless, it is important to continue your search.

Commercial insurance premiums can be a cause of friction. Would you buy a commercial auto policy if it only provided coverage on Saturday and Sunday?

If you could buy it at 10% of the competitor’s price would you do it?

Of course, you wouldn’t! This ridicules and silly example is used to get a point across. Price is significant! But only after you have determined that the policy is suitable for your business.

Insurance coverages change from one policy to the next

Coverage

There are many insurance agents, broke, s and carriers that sell on price alone. Each of them would love for you to believe that insurance is a commodity. Business owners beware. As the business owner or manager, it is your responsibility to make sure any business insurance policy being considered has the coverages that you need. When comparing multiple policies, make sure that they are on par with each other. It is the agent’sjob to provide a quote that is comparable to your current coverages. However, it is your business that will bear the brunt.

Great insurance agents don’t sell, they inform and advise. First, they take the steps to understand the prospective business. And hopefully, an understanding of the risk aversion of the prospect. After generating quotes and putting together a proposal. The question of price can now be considered. By interacting with the insured, risk management decisions can be made incorporating both coverage and price information.

Great insurance quotes don’t use deceptive practices to alter the relative value. The following are just a few ways that we’ve seen this attempted in the past:

BEWARE: If your deductible has a % sign and not a $ sign.

• DeductibleChanging a deductible from $500 to $1,000 without consulting the client isn’t a smart thing to do. Watching your deductible and other factors, that make up your commercial insurance policy is wise.

By committing to review your insurance policy when quoting and at renewal time you will also avoid some more adverse outcomes. While the dollar-based deductible change is concerning, beware of any deductible expressed as a percentage. Anymore it’s not uncommon to see 1% or 2% deductibles, especially for the wind/hail deductibles. If the deductible were 1% of the loss, there would be no issue. But it’s not; a 1% deductible is based on the policy limit. So if you have an office with a $600,000 value or limit, the deductible is $6,000 at 1%/ $12,000 at 2%.

Assume you have a 2% wind/hail deductible. A windstorm hits that result in $8,000 in damages. At first blush, a 2% deductible on an $8,000 claim is $160??

WRONG!

Your deductible $12, 0000. You pay for all the repairs.

• Read your application. There are a lot of questions, people make mistakes, and even worse sometimes they assume. By signing the application, you are attesting to the accuracy of the information that is being provided. Down the road, supplying the insurance company with bad information may muddy things up.

• What does your General Liability say about you? Your Commercial General Liability premium is a result of what and how much you do. You should review both for accuracy. Consider the following.

You have the opportunity to be an insurance company. Today you can write a General Liability insurance to one business only. Regardless of your choice, you will receive a premium of $500.

Insurance starts with understanding risk

The first company you can insure is in the Tree Removal Business. They also do lawn-care, snowplowing, and building demolition. Their current policy indicates that they are in the lawn-care business. The owner argues that this is correct as 50% of their revenues come from mowing lawns.

We have great lawncare insurance options in KY, GA, SC, and IN

The second company is a Lawn Care Business? They mow lawns. Period!

Pick one. Remember, the premium will be the same regardless of your choice.

The point is you need to know what type of business your insurance policy says you are. What if you’re the first business?

Do you think he will be covered if a tree falls on a house?

How much? How much business you do is also important. Premiums for Commercial General Liability are primarily a function of what you do. What you do has multiple meanings. For example, the type of work you do, how often you do it, how many people help you, how long you’ve done it and how many losses you’ve had.

What will happen If your application states that you have a payroll of $34,000 when the truth is you have a payroll of $95,000?

Houston we have a problem!

After your policy has been in force for a full year, your insurance company will perform an audit. At this point, they will discover that your payroll is almost three times higher. What happens? They will send you a bill to offset the difference. Hold on. Things are about to get worse. After plugging your true payroll into their system, you will start receiving significantly higher bills. One last carpet bomb; you know have a policy that is costing $2,000 more per year than advertised. In hindsight, you now have to question your decision. What appeared to be a $400 savings appears to have cost much more than the policy with all the bells and whistles. Wow!

But this is not the end of the process; it is ongoing.

It doesn’t matter whether you’re trying to buy Georgia commercial insurance or South Carolina. Great insurance is a two way street between the agent and the business owner. Constant communication aimed at awareness and identification of ever-changing exposures. Feedback to this should come in the manner of risk transfer options. This should include their cost and some form of analysis. The end result gives the business owner the ability to make an educated decision.

Business Insurance that’s on target. TruePoint Insurance!

There is an answer to what is the best business insurance. Unfortunately, it isn’t as simple as the insurance company or that insurance agent. It is a function of where you live, what you do, and what you need in regards to insurance. The formula should be extended to what insurance companies you can access. The final factor may be the easiest place to get off track. It is critical that you find an agent or broker that is knowledge and transparency.

Spring is knocking at the door and with it the rising risk

of insurance claims. The number and severity of storms in Kentucky have grown

at an alarming rate. The average number of tornadoes in Kentucky over the last

five years is 28.7. The annual average going back to 1950 at 14.6 tornadoes per

year is roughly one half of the current experience.

Kentucky’s weather is so out of hand. Some have even suggested that we are now part of the infamous Tornado Alley. A 2018 report by LEX18 News said just that.

In 2018 Kentucky was hit by 604 wind and hail storms. Of these,

41 were tornadoes. That is up 43% from the previous five years and an even more

alarming 181% from the period 1950 through 2018.

US Government HARP project is commonly considered to be experimenting with weather control

While we cannot change the weather, we can reduce Kentucky

home and auto owner’s exposure to it. Insurance is not a commodity. There are

some that would like for you to think it is. Good insurance agents recognize

the importance of providing clients with the proper protection. That includes

responding to ever changing risks.

Storm Alert: Auto insurance awareness

Protecting your car from damages related to storms is

simple. Make sure you have comprehensive coverage checked. It provides coverage

for vehicles damaged by wind, hail or falling objects.

Every auto on the road must have liability insurance. But

the wheels of many high-value and antique cars may never touch the road. Do

these vehicles need liability insurance? Maybe not, and they may not need

collision coverage either. Let’s stop and think about the next move. Removing

comprehensive coverage may not be the smartest move. When insurance is dropped

on cars that are not driven, owners are still exposed to Mother Nature. Fire,

wind, hail and other risk can still damage the vehicle even when it’s garaged.

These risks are compounded during the spring.

Comprehensive coverage is relatively inexpensive. Relative to the potential loss, this coverage can be very cost effective.

Storm Alert: Home insurance Awareness

Each client’s unique needs determine the coverages required. However, there are several considerations that may have severe impact on anyone.

While tornadoes take center stage, it’s the hail storms that

lead the way when it comes to losses. While this statement may seem

insignificant it has major ramifications on insurance. Total loss or partial

loss. Tornado versus hail storm. A good insurance policy needs to work well

regardless.

What types of losses will your policy

cover? This is critical. If it is available to you, a special peril or all-risk

policy is what you want. As opposed to a basic form or broad form, the special

option provides superior protection.

You will have the option for Replacement Cost coverage or

Actual Cash Value (ACV). All other things being equal, you will receive a

higher payment if your policy pays Replacement cost.

Deductibles may seem a bit dull when compared to other

areas. You choose $500 or $1,000, big deal.

Not so fast!

Many insurance companies have been forced to alter risk

sharing practices. Beware, as some are no longer asking for a set dollar

deductible. Instead, you may find that your policy has a deductible that is 1

or 2%. At first blush, it sounds like a pretty good deal for the home team.

Again, beware! This 1 or 2% of the total and it’s not the total value of the

loss. Your deductible is based on the total value of your home. For example:

A homeowner has wind damaged roof

§

Estimates for the repair work come in at $1,500

§ The

home is valued at $600,000

§

There is a 2% wind/hail deductible

The $1,500 loss will be shared by:

§ The

homeowner paying $1,200

§ And

the insurance company $300

Spring storms bring

more than just wind and hail. Heavy rains can lead to various forms of water

damage. Be sure to discuss flood insurance and water backup coverage with your

insurance broker. Neither of these will be covered by a standard homeowner’s

policy.

Spring! It’s a wonderful season and our springs in Kentucky

are certainly hard to beat. I think about how much I loved spring as a child.

It was by far my favorite season.

As an adult the grandeur has diminished. How wonderful it

would be to experience spring through the eyes of child again.

What is keeping me from doing it?

Could it be as simple as the aided stresses of being an

adult?

If so, then we should all take the time to review our

insurance coverages before the wind starts to blow. This should go a long way

in reducing stress.

Take care of the insurance and you’re half way home. Of course the other biggie is your income taxes and there you’re on your own. Have fun!

Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get Directions

When you buy a home whether it is your first home or forever home, it is a major investment. For most families, it is the largest investment they will ever make. It needs to be protected so that you will always have a roof over your head, a place to call home. If your house is destroyed in a fire or other disaster, you want to be sure that you will be able to rebuild, to replace what you had before it was destroyed.

When you buy a home whether it is your first home or forever home, it is a major investment. For most families, it is the largest investment they will ever make. It needs to be protected so that you will always have a roof over your head, a place to call home. If your house is destroyed in a fire or other disaster, you want to be sure that you will be able to rebuild, to replace what you had before it was destroyed.

If you have a mortgage and your home is located in an area that has been identified by FEMA as a flood zone, chances are, you have been notified that

If you have a mortgage and your home is located in an area that has been identified by FEMA as a flood zone, chances are, you have been notified that