TruePoint Insurance is one of Georgia�s fastest growing insurance agencies. We are affiliated with SIAA, a network of over 5,000 insurance agencies across the US, who by joining together have increased their strength and stability...

High school proms are

early chances to participate in a formal event. It is also considered a chance

to act as a full-fledged adult. The event involves arranging a complete evening

of dining, dancing and socialization. However, just as much time should be

devoted to making the event as safe as possible.

It is almost inevitable

that a prom will involve serious exposure to alcohol or other intoxicants. The

evening also involves many young, inexperienced drivers who are excited about

making their way to pre and post prom activities. Sadly, these factors have

combined to make prom season dangerous. Serious traffic accidents often become

the main feature of what should be a night of joy.

Prom-goers and their

parents need to create a strategy for making prom night both memorable and

safe. Here are some tips:

Parents should get all activity details, including dinner and pre and post prom events

Confirm the night’s events with school officials and other parents

Consider arranging a safe, group post-prom activity where participants can be supervised

Clearly lay out your expectations to your son or daughter about acceptable behavior regarding their evening

Discuss all details about transportation, whether they are drivers or passengers

Be sure that communications are set up. If the child does not have a cell phone available, find out the numbers where he or she can be reached during different phases of the evening

If practical, consider arranging for a third party to handle transportation (limo or taxi service)

Consider an amnesty arrangement. In other words, let your child know that they can contact a parent for emergency transportation should something go wrong and, for that evening, they’ll be no lectures or punishments

Help your son or daughter make prom night a bright memory rather than a tragedy. Plan on making safety and fun everyone’s priority.

COPYRIGHT: Insurance Publishing Plus, Inc. 2017 All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

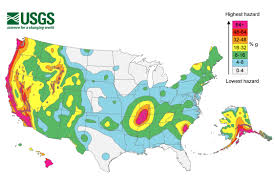

Most homeowners likely

know that, regardless where they live, they may be exposed to a catastrophic

loss such as flooding. It is definitely not restricted to coastal location.

However, the same cannot be said concerning earthquakes. It is much more likely

that only persons living in well-known earthquake areas (such as California and

Alaska) have a high awareness of its danger.

However, the danger of earthquake exists in several large areas of the United States, including a significant part of the Midwest. The New Madrid fault line crosses much of the Midwest, making states such as Indiana, Ohio, Illinois, Ohio, Kentucky Tennessee and Missouri vulnerable to earthquake catastrophe (particularly the latter two states). In the last decade, regular activity has been measured in this Seismic Zone.

A recent development is

affecting this source of loss. Though some questions remain, it appears that

the widespread practice of obtaining natural gas via the process of hydraulic

fracking may be triggering earthquakes in areas that had previously seen little

to no quake activity.

While many persons may

be exposed to the danger of earthquake, only a fraction of such property owners

carry the proper level of insurance. Basic homeowner coverage does NOT include

protection against earthquakes. Without purchasing specific earthquake

insurance, the only protection available for a policyholder is against limited,

consequential damage.

Example: The Johnsons

love their home on the outskirts of Juneau. While they’ve experienced a number

of minor earthquakes, in the few years they’ve owned the home: they did not buy

earthquake coverage. One day a quake occurs and severely damages their home.

The quake breaks a gas pipe and a fire erupts. The fire damage is covered

(though the quake damage is not).

Earthquake coverage is

typically quite affordable. It is generally available for a couple hundred

dollars per year to provide protection for a modest-sized home. While, even in

areas that are in earthquake prone, such losses are low probability; the

potential loss severity is so high that purchasing separate protection makes

sense. So shake up your insurance protection and avoid being totally shaken

down by a disastrous quake!

Insuring yourself against flood risk is a little different than other insurance policies. Many people mistakenly assume that they have flood coverage through their Fisherville, KY homeowners or renters policy, but they don’t. In order to protect yourself from flood risks, you need a specific flood insurance policy to cover related losses. While you can purchase federal flood insurance through an insurance agent, most flood insurance policies are administered through the National Flood Insurance Program (NFIP) and can be purchased by homeowners, businesses, and renters from an insurer who contracts with FEMA.

What Does Federal Flood Insurance Cover?

The maximum flood insurance coverage amount is $100,000 for the contents of your home and $250,000 for damage to the structure. Commercial flood insurance through the NFIP provides up to $500,000 for your building’s materials and $500,000 for damage to the structure. You can also buy what is known as “excess” coverage beyond the limits offered through NFIP through private insurers. Flood insurance coverage for the contents of your home and damage to the structure is sold separately. Coverage for personal property only applies to its cash value basis, whereas buildings are covered for replacement cost.

Federal flood insurance will cover direct physical losses caused by flooding and losses resulting from flooding-related erosion. For flood loss coverage for cars, ask your TruePoint Insurance representative for information about optional flood coverage through the comprehensive portion of your standard automobile insurance policy.

Buying flood insurance

If you have a mortgage and your home is located in an area that has been identified by FEMA as a flood zone, chances are, you have been notified that you need flood insurances. If not consider review the previous link regarding who needs food insurance. If you would like additional information, one of our agents will be more than happy to assist.

When buying flood insurance coverage, remember that almost 100 insurance companies offer NFIP policies. It’s easy to purchase. You can purchase a Federal flood insurance policy directly from an insurance professional. However, it does require a waiting period of 30 days before the policy takes effect.

Flooding can occur at any time and threaten your Fisherville, KY home, so don’t wait until the last minute to purchase it. Call TruePoint Insurance today for more information about protecting yourself from the risks of flooding.

It depends! Finding the best business insurance for many small businesses can be a challenge. Most small business owners in Kentucky will see that they have multiple options. Generally, competition leads to lower prices for canny consumers. With that said, commercial insurance is not a commodity and finding the best value may take a little effor.

Prices paid for Kentucky business owners’ insurance may range widely. Commercial insurance rates in Georgia and South Carolina are no different. Chances are, the more unique your business is, the tougher it will be to find a great deal on commercial insurance. Ferreting through the long list of products makes it difficult.

Insurance Options

To find the best commercial insurance for you, start by reviewing your options. Insurance companies do not write insurance in all states. It’s not uncommon to see a company provide great rates to business in one state, but for some small businesses, you will find that they don’t have a lot of options. Auto dealerships, certain trucking classes, and roofers are good examples. Regardless, it is important to continue your search.

Commercial insurance premiums can be a cause of friction. Would you buy a commercial auto policy if it only provided coverage on Saturday and Sunday?

If you could buy it at 10% of the competitor’s price would you do it?

Of course, you wouldn’t! This ridicules and silly example is used to get a point across. Price is significant! But only after you have determined that the policy is suitable for your business.

Insurance coverages change from one policy to the next

Coverage

There are many insurance agents, broke, s and carriers that sell on price alone. Each of them would love for you to believe that insurance is a commodity. Business owners beware. As the business owner or manager, it is your responsibility to make sure any business insurance policy being considered has the coverages that you need. When comparing multiple policies, make sure that they are on par with each other. It is the agent’sjob to provide a quote that is comparable to your current coverages. However, it is your business that will bear the brunt.

Great insurance agents don’t sell, they inform and advise. First, they take the steps to understand the prospective business. And hopefully, an understanding of the risk aversion of the prospect. After generating quotes and putting together a proposal. The question of price can now be considered. By interacting with the insured, risk management decisions can be made incorporating both coverage and price information.

Great insurance quotes don’t use deceptive practices to alter the relative value. The following are just a few ways that we’ve seen this attempted in the past:

BEWARE: If your deductible has a % sign and not a $ sign.

• DeductibleChanging a deductible from $500 to $1,000 without consulting the client isn’t a smart thing to do. Watching your deductible and other factors, that make up your commercial insurance policy is wise.

By committing to review your insurance policy when quoting and at renewal time you will also avoid some more adverse outcomes. While the dollar-based deductible change is concerning, beware of any deductible expressed as a percentage. Anymore it’s not uncommon to see 1% or 2% deductibles, especially for the wind/hail deductibles. If the deductible were 1% of the loss, there would be no issue. But it’s not; a 1% deductible is based on the policy limit. So if you have an office with a $600,000 value or limit, the deductible is $6,000 at 1%/ $12,000 at 2%.

Assume you have a 2% wind/hail deductible. A windstorm hits that result in $8,000 in damages. At first blush, a 2% deductible on an $8,000 claim is $160??

WRONG!

Your deductible $12, 0000. You pay for all the repairs.

• Read your application. There are a lot of questions, people make mistakes, and even worse sometimes they assume. By signing the application, you are attesting to the accuracy of the information that is being provided. Down the road, supplying the insurance company with bad information may muddy things up.

• What does your General Liability say about you? Your Commercial General Liability premium is a result of what and how much you do. You should review both for accuracy. Consider the following.

You have the opportunity to be an insurance company. Today you can write a General Liability insurance to one business only. Regardless of your choice, you will receive a premium of $500.

Insurance starts with understanding risk

The first company you can insure is in the Tree Removal Business. They also do lawn-care, snowplowing, and building demolition. Their current policy indicates that they are in the lawn-care business. The owner argues that this is correct as 50% of their revenues come from mowing lawns.

We have great lawncare insurance options in KY, GA, SC, and IN

The second company is a Lawn Care Business? They mow lawns. Period!

Pick one. Remember, the premium will be the same regardless of your choice.

The point is you need to know what type of business your insurance policy says you are. What if you’re the first business?

Do you think he will be covered if a tree falls on a house?

How much? How much business you do is also important. Premiums for Commercial General Liability are primarily a function of what you do. What you do has multiple meanings. For example, the type of work you do, how often you do it, how many people help you, how long you’ve done it and how many losses you’ve had.

What will happen If your application states that you have a payroll of $34,000 when the truth is you have a payroll of $95,000?

Houston we have a problem!

After your policy has been in force for a full year, your insurance company will perform an audit. At this point, they will discover that your payroll is almost three times higher. What happens? They will send you a bill to offset the difference. Hold on. Things are about to get worse. After plugging your true payroll into their system, you will start receiving significantly higher bills. One last carpet bomb; you know have a policy that is costing $2,000 more per year than advertised. In hindsight, you now have to question your decision. What appeared to be a $400 savings appears to have cost much more than the policy with all the bells and whistles. Wow!

But this is not the end of the process; it is ongoing.

It doesn’t matter whether you’re trying to buy Georgia commercial insurance or South Carolina. Great insurance is a two way street between the agent and the business owner. Constant communication aimed at awareness and identification of ever-changing exposures. Feedback to this should come in the manner of risk transfer options. This should include their cost and some form of analysis. The end result gives the business owner the ability to make an educated decision.

Business Insurance that’s on target. TruePoint Insurance!

There is an answer to what is the best business insurance. Unfortunately, it isn’t as simple as the insurance company or that insurance agent. It is a function of where you live, what you do, and what you need in regards to insurance. The formula should be extended to what insurance companies you can access. The final factor may be the easiest place to get off track. It is critical that you find an agent or broker that is knowledge and transparency.

Spring is knocking at the door and with it the rising risk

of insurance claims. The number and severity of storms in Kentucky have grown

at an alarming rate. The average number of tornadoes in Kentucky over the last

five years is 28.7. The annual average going back to 1950 at 14.6 tornadoes per

year is roughly one half of the current experience.

Kentucky’s weather is so out of hand. Some have even suggested that we are now part of the infamous Tornado Alley. A 2018 report by LEX18 News said just that.

In 2018 Kentucky was hit by 604 wind and hail storms. Of these,

41 were tornadoes. That is up 43% from the previous five years and an even more

alarming 181% from the period 1950 through 2018.

US Government HARP project is commonly considered to be experimenting with weather control

While we cannot change the weather, we can reduce Kentucky

home and auto owner’s exposure to it. Insurance is not a commodity. There are

some that would like for you to think it is. Good insurance agents recognize

the importance of providing clients with the proper protection. That includes

responding to ever changing risks.

Storm Alert: Auto insurance awareness

Protecting your car from damages related to storms is

simple. Make sure you have comprehensive coverage checked. It provides coverage

for vehicles damaged by wind, hail or falling objects.

Every auto on the road must have liability insurance. But

the wheels of many high-value and antique cars may never touch the road. Do

these vehicles need liability insurance? Maybe not, and they may not need

collision coverage either. Let’s stop and think about the next move. Removing

comprehensive coverage may not be the smartest move. When insurance is dropped

on cars that are not driven, owners are still exposed to Mother Nature. Fire,

wind, hail and other risk can still damage the vehicle even when it’s garaged.

These risks are compounded during the spring.

Comprehensive coverage is relatively inexpensive. Relative to the potential loss, this coverage can be very cost effective.

Storm Alert: Home insurance Awareness

Each client’s unique needs determine the coverages required. However, there are several considerations that may have severe impact on anyone.

While tornadoes take center stage, it’s the hail storms that

lead the way when it comes to losses. While this statement may seem

insignificant it has major ramifications on insurance. Total loss or partial

loss. Tornado versus hail storm. A good insurance policy needs to work well

regardless.

What types of losses will your policy

cover? This is critical. If it is available to you, a special peril or all-risk

policy is what you want. As opposed to a basic form or broad form, the special

option provides superior protection.

You will have the option for Replacement Cost coverage or

Actual Cash Value (ACV). All other things being equal, you will receive a

higher payment if your policy pays Replacement cost.

Deductibles may seem a bit dull when compared to other

areas. You choose $500 or $1,000, big deal.

Not so fast!

Many insurance companies have been forced to alter risk

sharing practices. Beware, as some are no longer asking for a set dollar

deductible. Instead, you may find that your policy has a deductible that is 1

or 2%. At first blush, it sounds like a pretty good deal for the home team.

Again, beware! This 1 or 2% of the total and it’s not the total value of the

loss. Your deductible is based on the total value of your home. For example:

A homeowner has wind damaged roof

§

Estimates for the repair work come in at $1,500

§ The

home is valued at $600,000

§

There is a 2% wind/hail deductible

The $1,500 loss will be shared by:

§ The

homeowner paying $1,200

§ And

the insurance company $300

Spring storms bring

more than just wind and hail. Heavy rains can lead to various forms of water

damage. Be sure to discuss flood insurance and water backup coverage with your

insurance broker. Neither of these will be covered by a standard homeowner’s

policy.

Spring! It’s a wonderful season and our springs in Kentucky

are certainly hard to beat. I think about how much I loved spring as a child.

It was by far my favorite season.

As an adult the grandeur has diminished. How wonderful it

would be to experience spring through the eyes of child again.

What is keeping me from doing it?

Could it be as simple as the aided stresses of being an

adult?

If so, then we should all take the time to review our

insurance coverages before the wind starts to blow. This should go a long way

in reducing stress.

Take care of the insurance and you’re half way home. Of course the other biggie is your income taxes and there you’re on your own. Have fun!

At TruePoint Insurance, agents help the residents of Fisherville, KY find insurance that meets their unique needs. We approach the client’s life insurance needs in the same manner.

Term life is an excellent choice for individuals who want to make sure that their final expenses are covered. It’s also an option if you want to have the policy mature within a specific period. A term life policy offers a variety of benefits that other types of life insurance don’t.

Specific Time Frame

Term life insurance is written for a specific number of years. Each payment is used to add equity to the policy until it matures at the end of the designated term. Term life policies can be written for 10, 20, or 30 years, depending on how big the plan is and how much you want your monthly premiums to be.

While Life and Universal Life Build Equity, Term Life DOES NOT

Whole and universal life policies are often referred to as permanent life insurance. The term permanent life relates to the fact that these policies do not have an expiration. In addition, the permanent policy develops equity which continues to grow as you make payments.

While the cash value grows slowly at first, once the equity has reached a certain amount, you may have the option to borrow against it. This is an excellent option if you have an emergency when you need access to cash. You can then pay the loan back by paying an additional payment every month.

The drawback to permanent policies: A Significantly Higher Premium

Lower Payments

The fact that term insurance policies don’t guarantee to ever pay the a penny is a negative for many. To answer the question of term or permanent life insurance you should start by asking yourself two questions: 1) As your progress through the various stages of life, will your life insurance needs change? 2) Is a permanent life insurance policy the best investment vehicle available to you?

It is a common belief that young families receive the greatest benefits of life insurance. There are many reasons that support this argument. While this age group is least likely to collect from a term insurance policy, the risk of not having protection is by far the greatest.

Young couples have may have a lot of balls in the air. Couples with children have legitimate concerns regarding their wellbeing should something happen to one or both of the parents. Increased demand for insurance among young couples can also be magnified if one spouse is the primary breadwinner.

The inflated insurance demands will in many cases be short lived. As children leave the nest insurance needs decline. Over time savings increase, further reducing the demand for life insurance.

It is normal that insurance needs are greatest for young families. It is also normal that young families have less disposable income. The lower premium associated with term life is often a much better fit for families that are just getting started,

While the primary benefits of a term policy is the lower monthly premiums Permanent polices act as both an investment vehicle and an insurance policy. For years the relative value of Term Life has been debated. Proponents argue that consumers should buy life insurance from companies specializing in such and allocate investment monies to those providing professional investment services. For years the call to action for this group has been ” Buy term and invest the rest.”

If you live in the Fisherville, KY area and have questions concerning term life insurance, call the agents at TruePoint Insurance and schedule an appointment. They will go over all of your questions and make sure you have the answers you need to make an informed choice.

We

have some great news to share. Tammy Rue, a life long resident of Anderson

County is now a part of the TruePoint team and we are excited.

Tammy has spent over 21 years helping individuals and businesses in Anderson County with their insurance needs. Finding individuals with deep local roots that also have extensive insurance experience doesn’t happen often. So it didn’t take long for us to realize the impact that Tammy could have. Going forward she will play a big part in our efforts in Lawrenceburg. too.

Drop by our Eagle Lake location this Friday, February 8th to help us celebrate this great addition to our team. Download

If you are the owner of a business that provides services to clients or the public, you may wonder if you need insurance, especially if you operate from home. All businesses that provide a service should have some level of coverage, even if it is liability coverage.

Businesses Providing A Service

If your company or organization provides a service to people, you need protection. You never know when you or someone you work for will be injured or suffer a loss. You can be held accountable for any incidence, and it can cause financial devastation without the right coverage for your market. Some businesses that need reliable coverage include lawn services, repair services, home health, in-home daycare, and more. Speak with an insurance expert to find out what type of coverage suits your business needs and make sure you don’t have costly gaps.

Working With An Expert

Always choose an agency that has expert agents when it comes to commercial insurance. They will help you find security and peace of mind with high-quality insurance products that protect you from a variety of dangers an potential threats to you and your business. If you live around the Fisherville, KY area, you can trust TruePoint Insurance to guide you in the right directions and present options that you need.

Don’t take chances if you provide a public service. Something could happen at any time and can jeopardize your career and your financial situation unless you have the right insurance coverage. Call or stop by TruePoint Insurance, proudly serving the residents in and around the Lawrence and Fisherville, KY area. We will work with you to find a policy that fits your situation and answer all of your questions.

Whether you live in Louisville or Lexington or the surrounding communities, you’ll have no trouble finding a great body of water. The Kentucky River, Ohio River, Mississippi River, and many other’s present awesome waterways for Kentucky boaters.

Kentucky is also home to many great lakes. Near the cities of Benton, Murray, Cadiz, Princeton, and Eddyville you will find two of Kentucky’s treasurers. Kentuck Lake and Lake Barkley combine for over 340 sq. miles of beauty and fun for all kinds of water-related activities. Other notable Kentucky lakes include Lake Cumberland, Barren River Lake, Lake Laurel, Green River Lake, Cave Run, and Rough River Lake.

One of the most common questions boat owners ask is whether they need insurance, and what kind of boats require such insurance. Based on current state law, you are not legally obligated to invest in boat insurance. However, you leave yourself susceptible to a number of issues if you fail to invest in such protection. Summer boating season will be here before you know it. Don’t make the choice to go without boat insurance without first considering the cost. Take a moment to continue reading, visit TruePoint boat and watercraft online or for a boat insurance quote call (502) 410-5089.

Consider What You Paid for the Boat

Does Kentucky require boat owners to have insurance? No. In Kentucky, it is legal to own and operate personal watercraft without insurance. That includes boat liability insurance. But before deciding to forgo watercraft boat insurance, first, consider what you paid for the boat. Now think how many opportunities there are for severely damaging your boat. On the way to the lake, you can relax a bit. As long as the boat is on a trailer being towed by your insurance truck or car, the liability exposure of the boat will be picked up by your auto insurance. Once off the trailer, the boat is your responsibility. During the process of unloading your boat, it’s possible for you to damage another boat. Just as easily you might also damage their truck, trailer, or even worse, another person. Once on the lake, there is an unlimited supply of exposures. Any of which might damage your boat. Damaging your boat and losing your entire investment would be bad enough, but if you are involved in an accident with another boat, you could potentially be out a boat plus buying a new one for the other party.

Your auto insurance coverage does not protect your boat. This means even if someone runs a red light and crashes into your boat during transport, your auto insurance coverage will not pay for it. Once on the lake, you will not only have property damage exposure, but you will no longer be protected by any form of boat liability insurance.

All Kinds of Boats Can Receive Coverage

If you’re able to take the watercraft out onto the water, then it can be protected with a form of boat insurance. Whether you have a bass boat or you have a houseboat you like to take out on the lake, all boats can be protected with boat insurance. Cheap boat insurance can be found, which makes it hard to justify putting on watercraft on the water without proper boat insurance.

Boats are expenses, but liability losses are the greatest exposure for Kentucky Boat Owners.

You are never legally required to obtain boat insurance. However, an accident on your way to the lake, on the lake, or even inside of your garage, may put your purchase at financial risk, and can even put you at risk of paying out due to liability issues. It’s easy to find out what kind of coverage options are available for Kentucky boat owners. All you need to do is give the team at TruePoint Insurance a call today.

Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get Directions

If you have a mortgage and your home is located in an area that has been identified by FEMA as a flood zone, chances are, you have been notified that

If you have a mortgage and your home is located in an area that has been identified by FEMA as a flood zone, chances are, you have been notified that

Whether you live in Louisville or Lexington or the surrounding communities, you’ll have no trouble finding a great body of water. The Kentucky River, Ohio River, Mississippi River, and many other’s present awesome waterways for Kentucky boaters.

Whether you live in Louisville or Lexington or the surrounding communities, you’ll have no trouble finding a great body of water. The Kentucky River, Ohio River, Mississippi River, and many other’s present awesome waterways for Kentucky boaters. But before deciding to forgo watercraft boat insurance, first, consider what you paid for the boat. Now think how many opportunities there are for severely damaging your boat. On the way to the lake, you can relax a bit. As long as the boat is on a trailer being towed by your insurance truck or car, the liability exposure of the boat will be picked up by your auto insurance. Once off the trailer, the boat is your responsibility. During the process of unloading your boat, it’s possible for you to damage another boat. Just as easily you might also damage their truck, trailer, or even worse, another person. Once on the lake, there is an unlimited supply of exposures. Any of which might damage your boat. Damaging your boat and losing your entire investment would be bad enough, but if you are involved in an accident with another boat, you could potentially be out a boat plus buying a new one for the other party.

But before deciding to forgo watercraft boat insurance, first, consider what you paid for the boat. Now think how many opportunities there are for severely damaging your boat. On the way to the lake, you can relax a bit. As long as the boat is on a trailer being towed by your insurance truck or car, the liability exposure of the boat will be picked up by your auto insurance. Once off the trailer, the boat is your responsibility. During the process of unloading your boat, it’s possible for you to damage another boat. Just as easily you might also damage their truck, trailer, or even worse, another person. Once on the lake, there is an unlimited supply of exposures. Any of which might damage your boat. Damaging your boat and losing your entire investment would be bad enough, but if you are involved in an accident with another boat, you could potentially be out a boat plus buying a new one for the other party. If you’re able to take the watercraft out onto the water, then it can be protected with a form of boat insurance. Whether you have a bass boat or you have a houseboat you like to take out on the lake,

If you’re able to take the watercraft out onto the water, then it can be protected with a form of boat insurance. Whether you have a bass boat or you have a houseboat you like to take out on the lake,  accident on your way to the lake, on the lake, or even inside of your garage, may put your purchase at financial risk, and can even put you at risk of paying out due to liability issues. It’s easy to find out what kind of coverage options are available for Kentucky boat owners. All you need to do is give the team at TruePoint Insurance a call today.

accident on your way to the lake, on the lake, or even inside of your garage, may put your purchase at financial risk, and can even put you at risk of paying out due to liability issues. It’s easy to find out what kind of coverage options are available for Kentucky boat owners. All you need to do is give the team at TruePoint Insurance a call today.