Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get Directions RVs mean time spent with family and friends on the open road. They represent adventures and the opportunity to develop lasting memories of time together. Just as you are required to insure your regular vehicle, you are also required by law to carry insurance on your RV. The situation that an RV represents is different than a normal vehicle and your insurance needs will also be different as well. Consider this; an RV is both a vehicle and a vacation home. When you are looking at various insurance options, it’s important to consider the pitfalls that you could encounter while you are away from home. The team at TruePoint Insurance serves the needs of Kentucky, Indiana, and Tennessee residents. They understand the unique challenges that RV owners face and can show you the options that are available to you.

RVs mean time spent with family and friends on the open road. They represent adventures and the opportunity to develop lasting memories of time together. Just as you are required to insure your regular vehicle, you are also required by law to carry insurance on your RV. The situation that an RV represents is different than a normal vehicle and your insurance needs will also be different as well. Consider this; an RV is both a vehicle and a vacation home. When you are looking at various insurance options, it’s important to consider the pitfalls that you could encounter while you are away from home. The team at TruePoint Insurance serves the needs of Kentucky, Indiana, and Tennessee residents. They understand the unique challenges that RV owners face and can show you the options that are available to you.

Policy Options

Just like an auto policy, there are many options, creating multiple alternatives to insuring a Recreational Vehicle. An RV policy can provide comprehensive, collision, and liability coverage. It will go further to provide coverage for the contents of the RV including equipment such as satellite dishes and awnings. It can also provide protection from accidents involving uninsured or underinsured motorists. You will want to make sure that the policy that you select also provides some roadside assistance. If it is not your primary residence and remains on your property most of the year, there may be discount options available.

Ok, that’s a bit of a stretch. I pretty sure your insurance will not cover you that far away from home. So how far can you go and still have RV Insurance coverage?

Ok, that’s a bit of a stretch. I pretty sure your insurance will not cover you that far away from home. So how far can you go and still have RV Insurance coverage?

Keep it in the United States and your good. Leave the country and you may not have coverage. For sure, if you are planning a trip with your RV to Mexico you will need to obtain a special policy. Otherwise, you will not have coverage while there.

Talk with your agent at TruePoint Insurance about potential savings if you only use the RV for a limited amount of time during a year. If you are in the Fisherville, KY area, feel free to stop by our office to discuss a policy and get a quote. Get ready to hit the road with TruePoint!

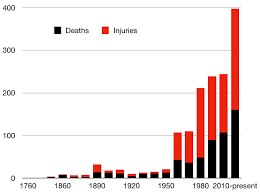

First, there is customer expectations. Insurance consumers may be under the impression that damage and injury created by shooters are covered. Second, the insurance market is fragmented over the issue depending upon how incidents are interpreted. Coverage may be sought from existing policies that individuals, commercial or non-profit entities may already carry, including General Liability, the Liability portion of Homeowners, or Workers Compensation. On the other hand, responsibility for harm due to a shooter may need to be covered by a form of professional liability policy as the obligation to protect against shootings may be considered as a failure to provide adequate security.

First, there is customer expectations. Insurance consumers may be under the impression that damage and injury created by shooters are covered. Second, the insurance market is fragmented over the issue depending upon how incidents are interpreted. Coverage may be sought from existing policies that individuals, commercial or non-profit entities may already carry, including General Liability, the Liability portion of Homeowners, or Workers Compensation. On the other hand, responsibility for harm due to a shooter may need to be covered by a form of professional liability policy as the obligation to protect against shootings may be considered as a failure to provide adequate security.

Business owners have a lot at stake when it comes to determining whether persons connected with their ventures are employees or independent contractors. The largest issue with making this determination involves taxes and insurance.

Business owners have a lot at stake when it comes to determining whether persons connected with their ventures are employees or independent contractors. The largest issue with making this determination involves taxes and insurance.

Because of the position held by policyholder/insureds and insurance companies, the classification of workers is often in conflict as insureds desire liberal coverage and insurers wish to restrict protection to qualified persons. However, both parties are best served when worker classifications are clear. Premiums charged to policyholders are based on correctly recognizing the parties eligible for coverage. Proper classification keeps coverage affordable and makes the insurance process more efficient. Coverage involving employees should be connected to an applicable business that employs them. Coverage involving independent contractors should be connected to the contractors. In other words, they should secure their own, separate coverage.

Because of the position held by policyholder/insureds and insurance companies, the classification of workers is often in conflict as insureds desire liberal coverage and insurers wish to restrict protection to qualified persons. However, both parties are best served when worker classifications are clear. Premiums charged to policyholders are based on correctly recognizing the parties eligible for coverage. Proper classification keeps coverage affordable and makes the insurance process more efficient. Coverage involving employees should be connected to an applicable business that employs them. Coverage involving independent contractors should be connected to the contractors. In other words, they should secure their own, separate coverage.