TruePoint Insurance is one of Georgia�s fastest growing insurance agencies. We are affiliated with SIAA, a network of over 5,000 insurance agencies across the US, who by joining together have increased their strength and stability...

Auto insurance in Fisherville, KY can be difficult to really understand on a deeper level. Ultimately, you don’t just need to know the general definitions and broad terms of coverage that you have. What you really need is in-depth details about what exactly will happen if something does occur. TruePoint Insurance wants you to know a few things before settling on a carrier for your vehicle.

Auto Insurance Is About You

Your auto insurance has everything to do with what you do. Whether you drive all the time or just a couple of times a week, your policy is tailor-made to fit you. This can be difficult to grasp at first, especially when it seems like one quote is the same as the next.

You Should Look Carefully

A lot of auto insurance carriers will make decisions that you didn’t necessarily expect, which can make the actual terms of your coverage difficult to process. This is why it’s necessary (if not convenient) to really over the terms of your coverage if you live in Fisherville, KY.

Your Partner Matters

Some insurance carriers are responsive in a crisis. They have a team that’s standing by to help you understand where you stand when something happens. But other carriers simply don’t have those resources, or the staff simply isn’t interested. If you truly want to understand your auto insurance policy, you need more than just promises. You need someone who’s going to really explain it to you.

TruePoint Insurance understands just how overwhelming and frustrating it can be to really look over the details of your policy. We understand why so many people choose based on financial considerations rather than the actual coverage that they need. Gives us a call today to see how we can help.

Comprehensive auto insurance is an excellent option for individuals who are purchasing new vehicles, as well as for those who cannot afford to replace their vehicle if it is lost to collision, theft, or natural disaster. Residents of Fisherville, KY and surrounding areas who are interested in learning about their comprehensive insurance options can consult a TruePoint Insurance agent to learn if this coverage is the right option for them.

Comprehensive auto insurance covers losses aside from simple collisions, typically including theft, fire, natural disaster, civil unrest and rioting, and the vehicle colliding with an animal such as a deer. If you live in an area where you may experience one of these situations, it may be wise to consider adding comprehensive auto insurance to your package. This will help ensure that you’re fully protected if an unfortunate event occurs.

If you’re purchasing a new vehicle, it’s often common for the lender to require that you carry comprehensive auto insurance due to the value of the vehicle. This helps protect both you and the lender in case of an accident or theft. You may find that you feel more secure, overall, when you carry this type of auto insurance no matter the age of your vehicle. Comprehensive coverage helps ensure that you’re protected no matter what happens, making sure that you can pay to have your car or truck repaired or even replaced as necessary.

When you’re deciding what type of automobile insurance to carry, there are numerous decisions to be made. Consult a friendly representative at TruePoint Insurance to learn more about the best type of coverage for your specific situation. We proudly serve the Fisherville, KY area and are happy to speak with you about the insurance coverage that’s best for you and your family, depending on the vehicles you have and the situations that you frequently find yourselves in.

Condo owners who live in Fisherville, KY may be at a loss of what to do if a neighbor causes damage to their personal property or condo. The agents of TruePoint Insurance can help navigate the process. Owning a condo is similar to owning a traditional home, with one exception. Condos are connected much like apartments. This means the negligence of a neighbor can result in property damage to your condo.

Registering a Complaint

If your condo or personal possessions are damaged due to a neighbor’s neglect, you will need to file a complaint with the property owner where your condo is located. It will be up to them to determine who caused the damage and who will eventually be held responsible for paying for any repairs that need to be made. Your insurance agent will work with the property owner to determine when repairs can be made.

Covering the Damage

In many cases, your insurance company will pay for the repairs to be made so that your condo can be returned to its original state as soon as possible. Both insurance companies will work together to ensure that the responsible party is held accountable for the damages that were caused. This is also true for accidents involving any type of injury that is caused by a neighbor or the primary property owner.

Fisherville, KY condo owners don’t have to stress over their insurance needs. By calling the agents at TruePoint Insurance, they can get all of their important questions answered. The agents understand the frustration of condo ownership, especially when it comes to certain types of risk. Call today to speak to an agent and get the answers you need.

For those that live in the Fisherville, KY area, owning a motor home can be a great option. When you have a motor home, you are going to have a vehicle that will allow you to drive around and tour the rest of the country. At the same time, it will also give you a place where you can relax and sleep when not on the road. If you are going to get a motor home, it is important that you get the proper insurance. There are several situations when someone should get insurance coverage for their motor home.

When Looking for Proper Coverage

One of the situations when someone shoudl get motor home insurance is when they want proper coverage for their asset. A motor home is a unique asset in that it is a combination of a home and a vehicle. Due to this, you need to have insurance coverage that reflects this. With a motor home insurance policy, you can receive the insurance coverage that you need.

When Taking out a Loan

You will also need to get motor home insurance if you take out a loan to buy the asset. A motor home can be very expensive to buy and using a loan makes sense for many people. If you do take out a loan, it is important to comply with the lender’s insurance requirements.

If you are looking to get insurance for your asset in the Fisherville KY area you should reach out to the team at TruePoint Insurance. When you do speak with the team at TruePoint Insurance, you are going to learn a lot more about how you can protect your motor home with an insurance policy. They can then help you get into a proper policy that meets your needs.

Strong listening, oral, and written communication skills

Goal oriented, highly motivated, and resourceful to achieve results

Ability to pay close attention to detail and accuracy

Ability to create and maintain business relationships with prospects and policyholders

Proven track record of trustworthiness, dependability, and ethical behavior

Fundamental understanding of office technology used by small business

Experience and Education:

Customer Service Experience (prior experience preferred)

Knowledge of Personal Lines, Life Insurance, and/or Commercial Lines products (preferred)

Property and Casualty license a plus

High School Diploma or GED

Associates or Bachelor’s Degree (preferred)

Job Related Training/Licensing:

Must have the ability to obtain a Property and Casualty license within the first year of hire.

Responsibilities:

Provide service to the public and policyholders in a pleasant and courteous manner

Be able to communicate clearly and professionally

Prepare forms and endorsements when required

Perform Billing and Customer Service duties in a timely and efficient manner

Meet customer service goals and assist with marketing goals

Be able to successfully navigate our Agency Management System and Carrier Websites

Perform other related duties as assigned

Pay and Benefits:

Salary will be based on experience, with the ability to advance based on performance and license. There will be an initial 90-day evaluation period to determine compatibility, salary increases, and bonus options. Interested Candidates should send a resume to New job Candidate Pooler GA.

There are many advantages to renting a home in Fisherville, KY as opposed to buying. You have greater freedom to move when you want and less financial responsibility. You also have the benefit of purchasing renters insurance to protect your valuables. Renters coverage is practical, affordable, and flexible, making it a smart investment in protecting your assets. Here’s how a renters policy from TruePoint Insurance can work for you.

Protection for Personal Belongings

Whether you’re renting a house, apartment or condo, chances are your landlord will have insurance to protect his property. His coverage, however, doesn’t include your belongings. By purchasing a renters policy, you can get the insurance protection you need.

Renters insurance offers various types of protection to protect you from financial loss. Property coverage protects your belongings. If your rental home is broken into and valuables stolen, property coverage helps cover their replacement cost. It also covers your goods if they’re damaged by vandalism, fire, water due to leaky pipes and other disasters.

Protection against Liability Claims

As a renter, you’re responsible for accidents that occur on your rental property. If someone gets injured while visiting your Fisherville, KY home, you could be held liable for his medical costs. Liability insurance covers accidental injuries to protect your personal funds. It also covers accidental damage to visitors’ personal property.

Protection against Loss of Use

If your rental home is damaged by fire, tropical storm, or other disaster and you have to live somewhere else temporarily while the house, condo or apartment is being repaired, loss of use coverage helps cover these extra costs. This includes hotel bills, restaurant bills, transport bills, etc.

These are just a few ways renters insurance in Fisherville, KY can work for you. To purchase a renters policy, call or visit TruePoint Insurance today.

We all know the difference between a truck and a car. Right?

The Thing; Car, Truck or ??

For most of my life, that was a straight forward question. Along comes the SUV and, more recently, the crossover, the once black and white responses it a lot grayer.

Here’s the good news.

Has your insurance agent ever asked if you needed, car or truck insurance? Probably not.

Since Cars, Trucks, and SUV’s are all insured by the same policy, there is no need to ask. However, You will be asked to provide your vehicles VIN. This will give the insurance company the information they need.

Delivery Trucks considered Commercial

Who needs a Commercial Insurance Policy?

Business Autos cannot be adequately protected with a Personal Auto Policy. A commercial policy of some form must cover these vehicles.

Who decides whether my vehicle needs commercial auto coverage?

Theoretically, any vehicle can be used for a business purpose. This requires extra effort from insurance carriers and agents as the work to provide adequate coverage.

I like to tackle that question from the other side. Who decides that a Personal Policy does NOT cover my vehicle?

Accurately communicating how you utilize your vehicle is critical. It allows your agent to confirm or deny that coverage exists for your situation.

Business Auto Insurance also Covers Personal Use

The Commercial Auto Policy is more flexible than Personal Coverage. While protecting your car at work, it can also safeguard automobiles during personal use. While Personal Auto covers only personal use of your auto.

If you use your vehicle in your business or profession, you may need Business Auto Insurance. In many cases, the need for Commercial Auto Insurance is obvious. Taxis, Tow Trucks, Delivery Vehicles, Cable Installers, Lawn Care providers are just a few examples.

What you say may be more important than what you drive.

How important is it for you to have your Company’s name, a business logo, or your phone number on your vehicle? I want my brand information anywhere and everywhere that I can afford to have it. While that may be great for business, it is also the first place I go to assist individuals regarding the need for commercial insurance. When vehicles have advertisements, there is little doubt. The question of commercial insurance or personal insurance is almost always resolved. If you’re driving a car with a business name or logo on it, you will almost always need a Commercial Auto Policy.

I occasionally drive my personal vehicle in work-related activities for my employer. Do I need Commercial Auto Insurance?

Remember, Business Auto Insurance is more flexible because it covers both commercial and personal use of your auto. Personal Auto Insurance covers your vehicle only when it is being used for personal activities.

Check with your agent before using your car or truck for any use other than personal.

Performing job-related duties while driving your car does not mean you need to run out and buy a Commercial Auto Policy. Your employer may have a more cost-effective solution. If you are asked to use your personal vehicle for work-related activities, you should first determine if the business has Hired & Non-Owned Auto Coverage in place. This coverage picks up what your personal auto policy coverage excludes. If you would like additional information on Commercial Insurance Policies or want to learn more about Hired & Non-Owned coverage, contact a TruePoint Commercial Specialist at (912) 330-1265.

An Rv is not just a luxury vehicle, but a home on wheels. During your tours in Fisherville, KY, many things can happen, including a road accident. Have you figured out how much loss that would be if you didn’t have any form of insurance?

Well, Rvs are pretty expensive. On top of that, they carry your valuables just like home. Speaking to an insurance expert in TruePoint Insurance can be a great idea as we will help you find out how much coverage is adequate for you.

Why do you need RV insurance?

We have already mentioned that RVs are like our homes on wheels, which means they carry a lot of value on the roads as well as when packed. While many states do not require drivers to have RV insurance, it makes sense to have a substantial amount of coverage in case anything happens to you out there. While they require ordinary driving skills, Rvs are bigger cars. You will need to make accurate estimations when driving or packing.

Factors that impact Rv insurance premiums

While insurance rates are different for every Rv owner, insurance companies use various criteria to calculate based on the information that you provide. Providing truthful information is a requirement as failure to do so can result in fines. Your Rv insurance premiums will be calculated based on the following factors:

The size of your RV

The age of the RV

Whether you are living in it or not

How long you will be using your Rv

Where you pack or store your Rv when not in use

Your location/address and many more

Your RV is a huge investment that needs to be protected at all costs. Large vehicles can cause significant damages and injuries to the parties involved. You don’t want to risk taking a tour in an uncovered car.

Do you need help buying Rv insurance? TruePoint Insurance can arm you with the right information to help you make a wise decision. Visit us at Fisherville, KY today.

Mobilehomes are vulnerable to serious damage from winds and storms since they are smaller and much lighter than stick-built or factory built homes. It is important to use reinforcements to make them more stable; such as tiedowns.

Tiedowns come in two basic types; over-the-top tiedowns and frame anchors. Over-the-top tiedowns are straps that resist lifting forces and minimize tipovers. They are usually used with single-wide mobilehomes. Strapping is placed with over the top of the roof or over the structure’s sides. Frame anchors are reinforcements that resist lateral forces, making a structure less vulnerable to sliding off supports

In order to stabilize a structure, the tiedowns must be properly anchored to a foundation, slab or the ground. Anchor types include the following:

· Hard Rock Anchor

· Concrete Slab Anchor

· Cross Drive Rock Anchor

· Drive or Barb Anchor

· Auger Anchor

· Disc Anchors

Straps and anchors have to be used properly and they have to meet various standards such as placement of anchors, anchor fittings, method of installation and ground/site conditions. When anchored to the ground, it may be necessary to make test its suitability as an anchor. If piers and footings are used they must be able to meet various requirements regarding weight support, dimensions, material quality, pier placement and other areas. Straps and anchors also have to meet requirements in order to be depended on to withstand the stresses winds and other forces.

Use of tiedowns varies by state, state regulations and soil type. Local building inspectors and mobile and manufactured home builder associations are excellent sources for anchoring and tiedown requirement information. Use of that valuable information, along with insurance, is great methods for fully protecting a mobilehome.

COPYRIGHT: Insurance Publishing Plus, Inc. 2017

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

Learn about flood insurance before the waters start to rise.

Who needs flood insurance? Many residents of Georgia and South Carolina are exposed to flood risk. Those living in coastal areas are like to be more at risk. Consider the following:

River Road – It seems wise that anyone living on River Road should check in to flood insurance.

Coastal Highway – Another great clue that suggests there is a heightened risk for flooding.

Lowcountry– Since floods occur in low lying area, it’s probably wise to consider flood insurance if you live in a region known as the Lowcountry.

Anyone with Lender Requirement

Does your home mortgage require flood insurance?

Your homeowner’s policy does not protect against flooding. For anyone needing protection from rising waters, a separate Flood Insurance policy is required. This policy will provide specific coverage if your home is damaged by a local flood.

Residents in Coastal Georgia and South Carolina may find that they are required to purchase flood insurance. This requirement is most likely come for a lender. Mortgage lenders know the potential impact of floods as well as which homes are at greatest risk. Due to this risk, borrowers with homes located in a FEMA identified flood zone will likely be required to maintain flood insurance.

Needs to Cover Against Risk

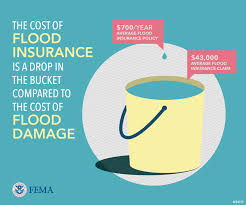

Flood Loss versus Cost. You do the math!

FEMA flood zones are divided into one of many categories. These categories or buckets identified the flood risk as very risky or a Special Flood Hazard Area (SFHA). Somewhat lower-risk areas are considered Moderate Flood Hazards. There are two moderate flood hazard groups; Zone B and Zone X (Shaded). Finally, the areas that are exposed to potential flooding yet have the least risk are identified as minimal flood hazards. This grouping also has twp categories; Zone C and Zone X (Unshaded)

Even if the risk is small, you should still consider getting flood insurance. Everyone should consider buying flood insurance. This includes those without a mortgage, and those not required to have flood insurance.

When you are looking to learn more about flood insurance in Georgia or South Carolina, you should speak with the team at TruePoint Insurance. They will make work hard to make sure that your decision is as simple as possible.

Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get Directions